#linear-algebra

2 messages · Page 230 of 1

Yes, you can do row operations

well what im saying is

we so far have only been taught Ra-Rb->Rb

Not Ra-Rb->Ra

and to then go off of that, if I followed the way of Row 3 - Row 2 -> Row 2 it would be -1-1 which would give me -2

And that is not the correct answer, it has to be +2

It still should have been a legal move

You're subtracting from the a row, so the result replaces the a row

and in this case the a row is row 3?

no, you're subtracting row 3 from row 2

so Ra(0,1,1,0,1) is row 2 and Rb(0,0,1,0,-1) is row 3 and that gives a new Ra

so Ra-Rb-> Ra

The number being replaced is is Row 2

why would it matter?

I get that

This problem is the first way seeing this

but why cant you do the other way

it gives -2 instead of positive 2

This problem has a unique solution

So my understanding is -2 is an incorrect answer

Could someone explain this explanation of hte solution better thanks!

The identity only has the eigenvalue 1

?

In a diagonal matrix, the eigenvalues are the values on the diagonal

Generally if you have a polynomial p(x), and a matrix A, if c is an eigenvalue of A, then p(c) is an eigenvalue of p(A)

So the eigenvalues of A^4 are lambda^4

Where lambda are the eigenvalues of A

Were A^4 the identity its only eigenvalue would be 1

But it isn't, so it can't be the identity

right

that's kind of a roundabout way of disproving the claim tbh

oh ok well i just used the complex diagonalizaiton and raised it to the 4th power xD

That's the same thing pretty much

This is a stronger claim though, since it works even when A isn't diagonalisable

k

Btw guys I need some help in finding a mistake in my working. I need to calculate XL given in the formula at the start of this page, and I'm given matrix A. The end result on the solutions is -(1/3)(e^(-3t)-1) on the top right corner of the final matrix, rest is correct. Where have I gone wrong?

Sorry i cant... exactly read your hand writing

Is it bad? I can try better

Basically I'm diagonalizing A because of the property of exponents of matrices

It makes things easier

also what is x(a)? or...?

But for some reason my answer is slightly different compared to solution

X(0) is just a multiplication value, I do nothing with jt

You can just ignore it

Seems like T^-1 is off by a minus sign?

It should be negative, ny handwriting was just confusing there

If you see under theres negative signs

Ic

If you are wondering about that property basically it works like this

Where T are the matrices that diagonalize A and Ad is the diagonalised matrix

So basically this saves me the pain of using Taylor expansion with matrices

Any ideas?

Can't seem to find a mistake

perhaps it might be because you did P^-1 D P but idk

Huh

Nah the formula is just the reverse

Maybe solution is wrong idk

Actually wait I do think it should be TDT^-1 in this case

@lone quail what did you do on the last step

Just multiplied by -1/3

Oh i see nvm i thought the squeezed in equals sign was an F xD

@lone quail it seems you did your matrix multiplication wrong

I just checked on matrixcalc and it seems doing Te^DT^-1 gives the solution in the answers

Could be

Where?

The other way doesn't make sense

wait

Since T is the COB matrix from the diagonalising basis to the standard basis

If you're sandwiching the diagonal matrix

PDP^-1 != P^- D P

It should be to the left

Where did I do my mistake?

This

It should be Te^Ad T^-1

You did the wrong factoriazation

Not the other way around

^

Nah im 100% sure thats the correct formula

Uhh

It's not

no

Multiply them

See if you get back A

From textbook

It says TAT^-1

It depends if you take T to be the COB from the diagonalising basis to the standard one or the other way around

...

Fedelisk

Take the diagonal matrix Ad

Multiply T^-1 Ad T

And see if you get back A

^

But im not multiplying by Ad here

Thats the issue

Thats the difference

I know the theory

It's not reversed when you do matrix exponents

It is here is the proof

They're originally taking TAT^-1 = Ad

In your case it's T^-1 A T = Ad

Noooo

I'm talking about the very top line

You have the order reversed in the very top line already

So it carries over

Guys to diagonalose a matrix is TAT-1

It's saying that given

A= T^-1 Ad T

Then the below formula holds.

But in your notation you have

A= T Ad T^-1

No because at the top Ad is the result

@lone quail

????

This part

In your notation

Yes that part not given that A = TAT^-1

Where is this?

This textbook/lecture nots are trash

The way you did the diagonalisation

Nope

Yes

That's not what I did

Ok the multiply T^-1 Ad T and see if you get A. The way you did the diagonalisation you get T Ad T^-1 = A

So the signs are reversed compared to the lecture notes

And that's where the confusion is coming from

Fedelisk you did the diagonalization for PDP^-1

and used P^-1DP

So you didn't do the factorizaiton correctly

If you don't believe me look up any lecture notes concerning matrix exponentiation

Yes but thats another formula, the diagonalised matrix in the middle

You are not listening

THOSE T ARE NOT THE DIAGONALISATION MATRIX OF THE MIDDLE MATRIX I USED

they are the T of a different matrix

Look at this

They are starting the process with the assumption I circled

Yes

In your case, your factorisation is yhe other way around

@lone quail if you are asking for help stop being such a bullheaded frog

So the proof will have the signs reversed

That is, the thing you call T, they would call T^-1

Guys just look at start and end of proof

That is the only difference

I've explained like 5 times by now. It's just the way you did the factorisation

Im not getting what you mean still

essentially you factorized A = PDP^-1 then tried to asume that PDP^-1 was equal to P^-1 D P which it is not

Where have I assumed that?

That's what im not getting

?

Roughly why?

It just makes it slightly easier to explain

@lone quail try computing the factorization you got.... like multiply it out

and see what you get

Which factorization?

ok so, when you take a matrix and set its vectors to the vectors of some basis B, then that matrix is the change of basis matrix from the basis B into the standard basis E right

so in your case, T is the change of basis matrix from the diagonalising basis B to E

Yes but what im doing here is T-1 x e^D x T

and T^-1 is the change of basis from E to B

except for hte middle matrix remove the e^blah

I understand where the confusion is coming from

and I'm trying to resolve that

Let me make it clear i'm talking about your specific example

not the textbook

So the matrix A_d is the same as the matrix A represented in the diagonalising basis B

So to get from A_d to A you'd have

A = T * A_d * T^-1

Since you need to go from E to B, then from B to E

No should be T-1 at start

Because Ad is already diagonalised

Ad is the matrix A in the basis B

So you need to undo

T^-1 takes us from the standard basis E into the basis B

then T takes us back to E

Yes but those Ts are not diagonalisation matrices anynire

Just change of base matrices

Nope

's the same thing

diagonalising matrices are change of basis matrices into a diagonalising basis

no you are

Ad is diagonalised

T takes you FROM B to E

A is non diagonalised

so T^-1 takes you from E (your starting point) To B

and then T takes you back

so you end up going from E to E

which is how A is represented

You agree that Ad = TAT-1?

Absolutely not

it's the wrong way around

if you still don't believe me

try multiplying it out

So what i'm getting at is that in your exercise A = T A_d T^-1, whereas in the textbook we have (Using different notation for clarity) B = P^-1 B_d P. So in the end they do get that e^B = P^-1 e^B_d P, but in your example it'll be e^A = T e^A_d T^-1 because of the same proof

great

glad we broke through in the end

np

consider the simplest invertible matrices

I think so but wouldn't know how to prove it. If you think about it tho, the determinant can sort of be imagined as an area in space, of a and b are different then the determinant of a^2-b^2 will not be 0

(it is not true)

So they can be not invertible?

There are some cases where it turns out not intervitble

Ah wait your right because because they can have the same determinant

oh haha!

fair enough, my counterexample was just taking A and B to be the identity

that was my instinctive thought too aha

a=b

or yea A=B

I mean if A and B got the same determinant

The result of the operation is prob 0

Maybe

for 1x1 yes

not necessarily in general e.g. diagonal matrices with det 1 but different entries to one another

spoiler it's still not true

just take A = -B

What if A^2 \neq B^2 tho 👀

probably still not true just slightly more annoying to come up with a counterexample to

det(a^2 - b^2) = det(a+b) det(a-b)

so we need a+b or a-b to have det 0 and so that should provide us with examples ig? i'll think

just take a= b+c with c being non invertible

yeah, try something like

gives infinite examples

yeah

But this is true as well

Can you give me an example?

just take say diag(2,0.5) and diag(0.5,2)

does that actually work, shiN

sorry but what's the link to this problem?

Just two random matrices I squared up

oh fair, sorry yeah that does work as a counter example

I was giving a counterexample to what fedelisk asked. It doesn't work for the original question

Btw those squared keep determinant 1

yes they do

Yeah

yea determinant is multiplicative

i see

if a matrix has determinant 1 then so does its square

Yeah

i was just worried as i thought you thought det(a^2 - b^2) = det(a^2) - det(b^2)

What I was saying in fact if the determinant is different from the start then a squared minus b squared is invertible

that's not true, as our counterexamples showed

It didn't?

e.g. a= diag(2,1) and b = diag(1,1) have different determinants

but a^2 - b^2 has determinant 0

Ok so if I square a matrix I square the determinant but I can't subtract?

yeah, det(a + b) is not det(a) + det(b) in general

I see

but det(ab) = det(a)det(b) as shin said which is cool

Yeah

If you think of determinants as areas it does make sense

Theres a nice visualization of 3blue1brown

hi guys, anyone can solve 8b ?

over what field?

don't know what formula to use. I can't solve it

matrix

whatever. The point is that when the matrix is multiplied by 3 times it will produce an identity matrix 3x3

i'd assume R then

perhaps a better question is - have matrices always been real so far in the class? do you know what a field is? etc

hmm, maybe just real number

sure

so, how to solve it ?

[-1 -1 0]

[ 1 0 0]

[-4 24 1]

seems to work (power 3 is indeed the identity matrix)

I don't see how to generate general solutions so I just searched random matrices until I found one with B^3 = I

I can see they have to satisfy B^2 + B + I = 0 for example (multiply by B - I to see that) but I wouldn't know anything useful

Maybe try to restrict B like a 2x2 matrix with B =

[1 0 0]

[0 a b]

[0 c d]

and search for 2x2 Matrices B' = [a b // c d] with B'^3 = I because they should get you B automatically with the condition

[ 0 -1]

[ 1 -1]

should do the trick as B' (again random matrices)

wow I've tried multiplying this one. and the result is true that B^3= I

sage: M = MatrixSpace(ZZ, 3)

sage: M

Full MatrixSpace of 3 by 3 dense matrices over Integer Ring

sage: M.identity_matrix()

[1 0 0]

[0 1 0]

[0 0 1]

sage: I = M.identity_matrix()

sage: while True:

....: i = M.random_element()

....: if i != I and i^3 == I:

....: print(i)

....: break

....:

[-1 -1 0]

[ 1 0 0]

[-4 24 1]

sage: a = Matrix([[-1, -1, 0], [1, 0, 0], [-4, 24, 1]])

sage: a^3

[1 0 0]

[0 1 0]

[0 0 1]

sage: M = MatrixSpace(ZZ, 2)

sage: I = M.identity_matrix()

sage: while True:

....: i = M.random_element()

....: if i != I and i^3 == I:

....: print(i)

....: break

....:

[ 0 -1]

[ 1 -1]

sage: a = Matrix([[1,0,0], [0,0,-1], [0,1,-1]])

sage: a^3

[1 0 0]

[0 1 0]

[0 0 1]

say thank you to SageMath I didn't do shit

right.. thank you so much SageMath and T0lgi

SageMath is a Program not a person

They do have a website where I downloaded it on my Computer (it's about 5GB in total, though) and actually an App on iOS (and probably other) making use of server computation (so you need WiFi)

Try to minimize usage from external programs because trying to find solutions by hand is also exercise by itself

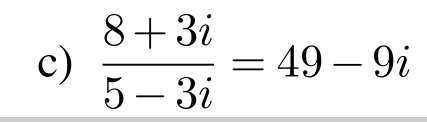

sorry I just need confirmation for an extremely quick question but

https://i.imgur.com/SJPvdE9.png this is incorrect, right?

(it wants me to get the Cartesian form a + bi)

im getting the answer 31/34 - (39/34)*i

Yeah it seems p wrong

(for future reference, wrong channel sorry, a question channel might be better :p)

no worriesss

Technically it's fine to ask about C in here, at least my first formal learning of C was in a LinAl course when we "rigourously" defined scalars

Companion matrix of x^3 - 1?

$ \begin{pmatrix} 0 & 0 & 1 \ 1 & 0 & 0 \ 0 & 1 & 0 \end{pmatrix}$

Mike Desgrottes

yep thats the natural linear algebra way to view this

alternatively you can look at it "algebraically" by looking for the matrix representation of a permutation in S_3 of order 3

which would give the same result

and i think is probably the best way to approach this

(if youre not familiar with the group terms, i just mean we're looking for a permutation ["swapping"] operation that "cycles back to the start" when applied 3 times)

(and then representing that with a matrix)

@opal mortar pinging in case this adds to your understanding, though your current answer is fine as well.

So the gradient of f transposed is a row vector right?

When I do it for a system of equations then, the n'th row of J should be the gradient of f_n?

But J is the Jacobian

And the Jacobian has the n'th column as the gradient of f_n

Should that be J transposed in C.11?

definitions of these quantities are not standard and depend on the book

transpose stuff as needed

if f(x) is scalar-valued, then grad(f(x)) as written there is a column vector, and you transpose it to get a dot product

so that the first order taylor approx is also a scalar quantity

it seems like the f_i(x) are the entries of a vector, let's call it F(x) (seems that's what they did, too)

so now if you have a vector F(x) and you take its derivative w.r.t. x, the derivatives are along the rows

so J is a matrix where each row contains the derivative of the corresponding f_i(x) w.r.t. x

seems your book follows the convention of "all vectors are column vectors" and "differentiation w.r.t. vector quantities go in the next available 'way' "

Oh rly fair lol, interesting

can someone help me how to simplify this

how much do you know about determinants?

When the prof wants to make sure you know the properties

@sinful knoll ???

I do know there are properities but none by heart :(\

oh yeah

and also det(A^T) = det(A)

i used wolfram alpha to calculate the SVD of this matrix

but, i dont understand how the last column of the U matrix is calculated?

wdym by "how"

do you wanna know about the algorithm for computing SVDs? otherwise just get a 4th vector orthogonal to the previous 3

yeah i dont really understand this svd stuff right now but, basically, you can compute an extra singular vector beyond whats in V and just use that?

what

U and V are, in general, not related at all to each other

matrices have left and right singular vectors

those depend on the original matrix's column space and left null space (left sing. vecs.) and row and null space (right sing. vecs.)

ok well

i am clearly way out of my depth here and fundamentally misunderstand all this

but just what i was reading said, to calculate each column in U, we multiply each singular vector in V with the original matrix A

which does indeed work looking at the wolfram output, except for the fact that the final column in U doesnt seem to have a corresponding singular vector to calculate it from, which is why i was confused

but yeah clearly i am totally misunderstanding this on some base level so i will try to read into it

well, since V is orthonormal, and a matrix M is decomposed into M = USV^H, when you multiply by the singular vectors in V (i.e. the right singular vectors), you get USV^HV = US

so the result is a matrix U times a rectangular matrix S with entries only along its main diag.

i think the best you can get this way is the set of vectors U_c that span the column space of the matrix

not the ones for the left null space

you can extend the vectors U_c into an orthonormal basis for R^m or C^m using gram schmidt tho

just generate random vectors of the correct size, check they're all linearly independent when put in a set with the vectors in U_c, and put the vectors U_c first when you do gram schmidt so that you modify the randomly generated vectors instead of the ones you already know are correct

ok thank you, i will look into it

what you were doing is related to the so-called "economy-sized SVD"

will $S ={x(a_1, a_2) + y(a_3, a_4) \mid x,y,a_i \in \bR}$ always be a subspace of $\bR^2$ if $(a_1,a_2)$ and $(a_3, a_4)$ are non parallel vectors?

CoolShot

your notation needs fixing right now

you do not want to quantify over all possible values of a_i in your set

as-is, what you have is an overly elaborate description of R^2

if you meant $S = { x(a_1, a_2) + y(a_3, a_4) \mid x, y \in \bR }$, with $a_i$ arbitrary but fixed, this will \textbf{always} be a subspace of $\bR^2$ even if $(a_1, a_2)$ and $(a_3, a_4)$ happen to be parallel.

Ann

nvm youre right i confused myself

even if they were parallel it'd be closed under vector addition and scalar multiplication and have a zero vector

so itd be a subspace

yup

ty

You can view this as essentially taking (a1,a2) and (a3,a4) and forcing S to be a subspace

'oh, if u and v in the set then so must xu + yv for all x,y in R? well let's just chuck them all in'

Numer d is not a vector space right?

because if u add x^3 with -x^3 = get somethign thats not in teh set?

the only sensible candidate fields are Z/pZ, but those end up failing distributivity

so no

(this isnt the most formal argument; for a more formal one, see https://math.stackexchange.com/questions/151850/prove-mathbbz-is-not-a-vector-space-over-a-field)

Mathematics Stack Exchange

This is an exercise from Chapter 3 of Golan's linear algebra book.

Problem: Show $\mathbb{Z}$ is not a vector space over a field.

Solution attempt:

Suppose there is a such a field and proceed by

another simple argument: observe that Z would necessarily be a 1-dimensional vector space since Z is generated additively by (1)

but a 1-dimensional vector space would necessarily have "itself" as a base field (upon fixing a basis)

except Z isnt a field

$A = \begin{pmatrix} 1 & 1 &\ 0 & 1 \end{pmatrix}$ is not, for example

potato

only eigenvalue is 1 and if Ax = x then we must have x being a multiple of (1,0) i.e. the eigenspace is 1 dimensional so not diagonalisable

There are nice types of matrices you can prove you can diagonalise (stuff like normal/unitary/real symmetric matrices) though

it is a crime that no one has mentioned jordan canonical form yet

this is also called a defective matrix and something worth knowing about symmetric matrcies is that they have orthognoal eigenvectors

canonical tteppa

Yea think so

So like if b=0 just show for any f,g in space then cf+g also integrate to 0, and if b not 0 u can find counterexample by taking day 2*f

Say*

is P the price vector?

in the exercise they asked me to determine the price vector with a system

but I wonder, that vector p that I have there is the vector of prices?

if you have no pivot columns that means all ur vars are free

so wouldnt that make it so that all b values would have solutions

What is meant by saying "a set of functions"?

What it sounds like

a set, containing functions

different functions

wiki "In mathematics, a function space is a set of functions between two fixed sets"

i'd be careful using the term "space" here since that usually refers to a set of functions with some extra structure (such as that of a vector space)

yeah... it's what it sounds like

the set of functions b/w 2 sets

so I'm reading about vector spaces "If S is a set, then F^S denotes the set of functions from S to F" but I just have a question in my mind, what function?

Any

all of them

Like, let's say we have 2 vector spaces V and W, then we can say the set of functions $W^V$ would be all functions who map vectors from V to vectors in W

Is this correct so far? At this point, can I do an epsilon delta proof? I'm not sure if it is the same for functions with complex domain.

Mosh

pick any norm, it's finite dimensional so they all give the same topology

yea I know, it

s just weird they didn't specify

wait actually you don't need a topology on V here nvm

I misread the problem

you can do smth like an epsilon delta proof but just using open balls in C instead of open intervals I think

just handwave and say "function jumps at an eigenvalue so it's discontinuous there"

if it's a linear algebra class i doubt you have to give the rigorous analytical details

maybe add that there are finitely many eigenvalues so there is a nbhd of lambda_0 in which it is the only eigenvalue

so clearly there is a discontinuity at that point

what is nbhd?

neighborhood

Ah, thanks. So I can find the delta neighborhood in my discontinuity proof.

Just self-teaching rn

yea, so it's constant at all points in that nbhd except lambda

where it jumps

actually if you're disproving continuity you don't actually need that

you want to show that there exists some $\varepsilon>0$, such that for all $\delta>0$, there is a point $x$ in the delta-nbhd of $\lambda$ such that $\abs{x-\lambda}<\delta$ but $\abs{f(x)-f(\lambda)}\geq \varepsilon$

ah true.

ShiN

where the first absolute value is complex

Does this check out at the end?

seems good

thanks for the help

np

just started my intro to linear algebra class... what does this question mean?

do i leave in REF or RREF?

Continue row reducing until you can read off the solution set

So i know this is an inconsistent solution set

for example, 7 you dont have to do anything else cause you can read off that there is no solution

Nope, however for 8 there is still work to be done

Oh ok

cause you can easily tell the system will row reduce to $[I|b]$

Mosh

so it will have a unique solution

If i put this into desmos I get that there is a common point of intersection

But my reduction work says that there are infinitely many solutions

what am i doing wrong?

sorry didnt see the ping: You further row reduce like I said

it doesnt

well you didnt link a video

copy pasting from mac doesnt show up

❖ A linear system Ax=b has one of three possible solutions:

- The system has only one solution.

- The system has no solution.

- The system has infinitely many solutions.

So, we have explained how to determine if a system of equations has the three types of solution which are a unique solution, no solution, or infinitely many solutions. Als...

there we go

i mean even from the thumbnail

yeah, that's different

oh ok

cause one of the columns in that example is free

how can I prove u+v belongs to W for u,v belongs to W.

ask yourself: is the sum of two singular matrices necessarily singular?

the answer should become obvious if you consider something like the identity matrix and how it can be written as a sum.

thanks

sup

Say I have 2 matrices, A and B, is there a way to find every possible result of matrix multiplication of A and B (ie. ABB, ABBAB, AAABBA, etc.) assuming that there's a finite set of results?

Gonna say no, cause there are an uncountable number of binary strings

There's a countable amount of finite binary strings though. The only case I can think of a finite number of possible products happening tho is when the eigenvalues are 0 and 1.

or -1

So, I want to calculate the determinant of the matrix

$$\begin{pmatrix}\vert & \ldots & 1 \ e_1 + e_n & \ldots & 1 \ \vert & \ldots & n-2\end{pmatrix}$$

For arbitrary $n$ ($e_i$ are the standard basis vectors). I suspect it always comes out to -1 but i'm not immediately seeing an inductive argument for it

ShiN

also eigenvalues seem to be a pain

any ideas?

the n-1 first vectors are $e_i+e_n$ and the last vector is all 1s except the last coordinate which is n-2

ShiN

Here's n=8 if that helps visualise it

I think maybe splitting it into the diagonal part and the part with only the row and column of 1s might make it easier? then you could use induction on that part

does it help to rewrite the last column as the sum of all the previous ones minus e_n?

me neither, i was just throwing the idea around

Ah ok

maybe rules of how the determinant of a matrix changes when you do column operations, for example

idk

😌

ok so actually using multilinearity it reduces to the last row just being -e_n

and now the matrix is lower triangular

aha

nice

thanks

the eigenvalues are always 1 with multiplicity $n-2$ and the last 2 eigenvalues are $((n-1)\pm \sqrt{(n-1)^2+4})/2$

Sven-Erik

matrixcalc gave me a different eigendecomposition for n=6

not really important tho

julia> A

6×6 Matrix{Float64}:

1.0 0.0 0.0 0.0 0.0 1.0

0.0 1.0 0.0 0.0 0.0 1.0

0.0 0.0 1.0 0.0 0.0 1.0

0.0 0.0 0.0 1.0 0.0 1.0

0.0 0.0 0.0 0.0 1.0 1.0

1.0 1.0 1.0 1.0 1.0 4.0

julia> eigvals(A)

6-element Vector{Float64}:

-0.19258240356725248

1.0

1.0

1.0

1.0

5.192582403567252

julia> [((n-1)+sqrt((n-1)^2+4))/2, ((n-1)-sqrt((n-1)^2+4))/2]

2-element Vector{Float64}:

5.192582403567252

-0.19258240356725187

oh wait the matrix I entered in matrixcalc was slightly different

by a column operation

not sure if that would affect the EVs

All EV can also be expressed explicitly

anyone know a visual learning instructor for intro to linear and differential equations. its a struggle, keep running into instructors that have a vibe of "dont ask questions, do it yourself". i think my only option is taking online and self teach.

you could check out the "Essence of linear Algebra" Playlist on youtube

has a lot of good visuals

Here to verify a question, it looks right to me but im not 100% sure ```

Given any nonzero vectors u and v, determine the scalar c so that the vector u + cv is perpendicular to v.

v * (u + cv) = 0

(v1,v2) * (u1 + c * v1, u2 + c * v2) = 0

v1(u1 + c * v1) + v2(u2 + c * v2) = 0

c(v1^2 + v2^2) + v1 * u1 + v2 * u2 = 0

c = -v1u1 - v2u2 / (v1^2 + v2^2)

If v and u were in 3 dimensions (question does not specify)

would

c = -v1u1 - v2u2 - v3*u3 / (v1^2 + v2^2 + v3^2)

be correct?

thx for taking the time to read this

$c=\frac{-(v\cdot u)}{\norm{v}^2}$

That looks right

Mosh

yes

yes

you can simplify it however

you don't need to write them as (v1,v2)

$v\cdot (u+cv)=0 \implies v\cdot u + v\cdot cv=0 \implies v\cdot u = -||v||^2c \implies \frac{-(v\cdot u)}{||v||^2}$

v.(cv) in the 2nd line

jswatj

Ann

$||v||$ vs $\|v\|$

oh, i had no idea

you can also do \Vert (capitalization matters)

\vec{}

nice

vector arrows

any recommendations for instructors at a community college?

alright thx, i just read this, ill write it in the simpler form

need help on a particular problem ... let me type out how far ive gone so far

so for 5a i would just do like

x1 + x3 = b1

-x1 + 2*x2 = b2

2*x1 + 3*x3 = b3

right?

for 5b am i bit confused. by solve it do they just mean put x1 x2 and x3 in terms of b? if they meant that then why doesnt it say so? would x3 = -b3 + 2*b1 be correct if this is the case

and for 5c i was gonna guess

3 0 -1

3/2 1/2 -1/2

2 0 -1

based off my answers from b.

is that right?

thanks

can a matrix with infinitely many solutions be consistent?

how does that work

i am confused

find the temperatures at 1,2,3 and 4

then solve the system

for example, $4T_1=10+20+T_2+T_4$

Mosh

which comes from examining node 1

okay

do that for all 4 nodes, and you'll have 4 equations in 4 variables

each temperature does not need to have a coefficient though right

or does it not matter

There is, it just doesnt affect T_1

It will help when writing the augmented matrix, but for 43 it doesnt matter

$4T_1-T_2+0T_3-T_4=30$ makes it clear the 1st row of $[A|b]$ will be $[4,-1,0,-1|30]$

Mosh

oh ok

@nocturne jewel correct me if im wrong but

T_2 would be (20 + 40 + T_1 + T_3) / 4 correct?

yeah sorry

forgot the average

i was just having difficulty understanding how to read the diagram

thank you though for your explanation

this isn't too hard

for 5b you can just put it in an augmented matrix and row reduce it accordingly

actually for 5c just write it out like they want u dont need to invert it

then pull out b and get the coeffecients for A^-1

i think what you have is right

if you row reduced properly

Can anyone explain how points P and Q end up as a vector?

one can use vectors to indicate positions, so-called position vectors

these vectors have tail at the prigin and head at the point

you see they took the coprdinates of p and q and directly put them into vectors. this is the same as doing e.g. p - (0,0)

coordinates and pos. vectors behave similarly to each other and the distinction is slight.

ok, i'd initially plotted them as follows. i've read that they don't have to start from 0 on a cartesian plane

tje what doesnt start at 0?

vectors dont have a location

you can assign a location to them if it helps you, but this is extra info

in this sense, you need to express the vector in terms of both the head and the tail

once you subtravt the 2, you habe a single vector with no location. you could place it anywhere on your plane if youd like

though it is customary to again set ita tail at the origin

how would one draw them graphically?

I got this... but doesn't seem to make sense cos the - signs are no longer there

This seems to conform to the answers

Q - P = Q + (- P) = - (Q - P)

youd need to look up how that plotter's vector() function works

cuz you see changing the order of P,Q changes the direction the vector points in

is this an exam? it seems to have points assigned to it

bout to ace his exam 🙏

with discord help

its a question from a sample question paper

what about the geometric discription

rotate x by an angle theta

range will be the sum of the vector and the rotated vector, ryt?

mhm. and well, that's a linear operation. now say the result is called y = Rx. what does x_0 + y do to y?

what does that mean geometrically

let's see it this way. Rx is some random vector. let's say we fix its length to 1. we still don't know its angle though, so for practical purposes, we can depict Rx as a circle with center at the origin.

what happens if we now add x_0 to Rx?

what happens if you add x_0 to every single point on a circle?

radius of circle changes?

try it yourself on a piece of paper. say the circle passes thru (0,1), (1,0), (-1,0), (0,-1), which a circle with radius one and center at the origin does

all of those points can be represented with position vectors

those are possible results of Rx

now add a vector x_0 = [2,2] to all of them

and draw the circle that passes through those points

what do you get

displaces the origin?

bingo

so you can describe this as first rotating the vector x and then displacing it

got it

now you can test the linearity yourself, but as a direct consequence of the displacement, 0 is no longer mapped to 0

this should already tell you if it's linear or not

alternatively, see whether T(v + w) = T(v) + T(w), which is a property that must hold if T is linear

thanks for the help

that's the take-home message

Can I ask a question here or is that not allowed?

It's about vectors and the problem is:

I know what to do if vectors c + d is a single vector and it goes from the initial point of vector A to the terminal point of vector B, but I'm unsure how to approach this problem because that isn't the case

Yes, that'll make the same vector but just pointing the opposite direction

yeah so now you can draw the vector -c + d onto that graph

Shouldn't -d be better than -c?

looking at the directions of the arrows

cant you straight up say c -2a = b + d

and simplify that

it's the same as ehat vee says, but without modifying any of the given vectors in the plot

Ahh. I was looking at the question wrong, I don't know why I kept thinking it was a=c-d-b

I understand now, since a has a scalar value of 2, and the question is looking for a by itself, we need to divide by 2.

How can you draw that conclusion that you can straight up say c-2a=b+d, can you elaborate a little bit? You're right but I just want to understand how you were able to make that deduction right away

you draw a line from where 2a and b meet to where c and d meet

or you imagine that line

follow -2a + c is the same as follow b+d

i feel like we imagine these differently though, so this just how i see it

alternatively, you could have also done: a + a + b + d = c by the process of vector addition (resultant vector is formed by connecting tail of first vector to the head of the last vector)

either way, u arrive at the same answer

many ways to imagine these

I see

either way, u arrive at the same answer

Well, thank you all for the generous help

as they said

vector addition sets vectors one after the other. the head of one is the tail of the other

subtraction instead joins the heads of two vectors, and the head of the resulting vector follows the classic vector = head - tail principle

how do i get rid of the bracket inverses in this (matrix btw)

just take the inverse of both sides

how?

by inversing both sides?

both sides of the equation?

im not sure how A^{-1} or C^{-1} showed up

B^{-1}D on the right side is correct

when you take the inverse on the left it just cancels out the inverse already there

you'd get N^{-1}A + C

you can also multiply both sides by the inverse of the LHS and see if that helps in any way

multiply both sides by tteppa

guys, im confusing with definition of dependent variables. can someone help me if its right or not?

if there is y that dependent on linear 3 variables (in this case with noted as x0, x1, x2) and some constant, is it posible i write this as below?

y = x0 + x1 + x2 + C

what was the definition given to you?

well, i was thinking on implementation (the question is just made by myself) on some data. there are 3 variables that plotted with 1 output varible, and all of them is shown graphicly linear

and statement above is my conclusion.

so you want to do a linear regression?

yes

you're close, but forgot possible scalars for the x_i

$y = \beta_0 x_0 + \beta_1 x_1 + \beta_2 x_2 + c$ i guess

Ann

oh nvm its just schur complement

you can usually take all the vector equations and just stack all the vectors on top of each other

you could build it that way

dual problems are usually formulated that way

you get a new problem with different constraints, and then make a huge inefficient matrix that you would never actually code

but looks nice on paper

R is presumably a correlation matrix, yeah?

hermitian positive (semi) definite

you can factor it

yada yada

B^H B

yea

what does the P_m (F) = span(1,z,..,z^m) notation mean here

and what is this saying:

you know what the span of a set of vectors is?

yep

the vectors are 1, z, z^2, ..., z^m

for example, you can construct any order 1 polynomial by considering linear combinations of 1 and z

i am confused because i dont know what it means for 1, z, z^2, .., z^m to be vectors, their variables in a polynomial expression with degree m

vectors in a vector space can be anything that satisfies the definition 😛

look at this example

can i see an example , yah

you know what a linear combination is, yeah?

yea

so let's say we have the vectors 1 and z

ok

order here means degree, yeah?

ah, i see

(where a and b are from F)

yep

you could also build an isomorphism to R^{m+1} if it helps you

some sort of correspondence between these monomials and canonical basis vectors

e.g.

for quadratic polys

so it's saying the set of polynomial functions with degree up to m that map F -> F can be expressed as span(1,z,..,z^m) ?

yes, cause polynomials are just linear combinations of monomials

yep

just open up your mind to what "vector" means

ok that helps

review the definition of vector spaces and subspaces and notice it's just a set of basic rules

vectors are just things that can have a notion of "adding" and "scaling"

literally anything that satisfies those rules is a "vector" in a very abstract sense

i am used to think of vectors strictly as F^n as oppose to any thing that satisfies the vector space axioms

that tends to be the first example one sees, indeed

but that makes a lot more sense

can you help break down what this is saying as well

is it saying polynomial functions are uniquely determined by their coefficients? i dont understand

what it is saying

yes

ok i see

Basically if I have $p(t)=\sum_{i=0}^{n-1}a_it^i$ then I can make an isomorphic map which maps $p(t)$ to $$[a_0,a_1,...,a_{n-1}]^T$$

Mosh

so if you have: a1 + a2 z^2 + ... + an z^m and b1 + b2 z^2 + ... + bn z^m, then in order for the two polynimials to be equal then a_i = b_is have the be equal?

yes

awesome, thank you

if p(z)=q(z), then constants must match, linear terms must match, etc

ok, that makes a lot more sense now thank you

that answers all my questions for now, thanks for all of the help

ok, so i think this is saying y, R are fixed, and saying that if t is varying, then min t = y^HR^-1 y must hold for the block to be PSD

maybe im not used to it but was hard to parse what the statment is saying...

i would need to read all of the context to know. idk what the goal is. estimate y? estimate R? get t?

yea, i think the context agrees

theorem is this

they basically break Y, which is fixed matrix into columns y_t

now, in here, why can't we have y^H R^-1 y < min|x|^2

you say that, but what you get is the minimum 2-norm solution for x

depending on how A looks, there might be no or infinitely many such x

true, this is only supposing there is some x?

they used tikhonov so i guess they want a smooth one

hm thnaks ill look it up

that R + \sigma I stuff

I think its ok to assume A full column rank here and theres a solution, so all is good

since the context is T(u) is toeplitz with decomposition A^HD^1/2 D^1/2 A

and applying there, y is in the span of A

Heya all, super sorry if I’m in the wrong channel here; it wasn’t a specific homework problem or anything and I think it has to do with la so I decided to put it here but does anyone know what this is?

I searched up Vandermonde Determinant and just saw a bunch of matrices?

Not sure how it would be calculated in this context,,,

do you know the general form of a vandermonde matrix? And do you know what a determinant is?

The general form of it is

$$ M =

\begin{pmatrix}

1 & a_1 & a_1^2 & \dots & a_1^n \

1 & a_2 & a_2^2 & \dots & a_2^n \

\vdots & \vdots & \vdots & \vdots & \vdots \

1 & a_n & a_n^2 & \dots & a_n^n \

\end{pmatrix}

$$

The usual time complexity of calculating a Determinant of a Matrix is usually $O(n^3)$, basically a polynomial of degree 3 with respect to the number of rows/columns of the Matrix.

The Vandermonde Matrix is a special form of Matrix that comes up in other areas in math and Vandermonde found a trick to calculate the Determinant of this certain form of a Matrix (which is $O(n^2)$). It's not that complicated as we got this as a homework problem but I'll spoil the result here

$$

\det M = \prod_{1 \leq i < j \leq n} (a_j-a_i)

$$

So for example, the Matrix

$$ M =

\begin{pmatrix}

1 & 1 & 1 \

1 & 2 & 4 \

1 & 4 & 16 \

\end{pmatrix}

$$

(why is this in the vandermonde form?) has the Determinant

$$\det M = \prod_{1 \leq i < j \leq 3} (a_j-a_i) = (4-2)(4-1)(2-1) = 6$$

The sequence looks at increasing matrices. The matrices get solely defined by the second column (hope that's clear). The sequence asks $a_1, a_2, a_3, \dots$ to be $1, 2, 4, \dots$ so $a_i = 2^{i-1}$. Since we know the Determinant of these matrices, we can rewrite the series as

$$

\det M = \prod_{1 \leq i < j \leq n} (2^{j-1}-2^{i-1})

$$

So the sequence would be

$$1, (2-1), (4-2)(4-1)(2-1), (8-4)(8-2)(8-1)(4-2)(4-1)(2-1), \dots = 1, 1, 6, 1008$$

Hopefully you can see by looking at what factors gets added (or here multiplied) at each step that each term divides its successor. The second note that $2\cdot v(n+1)/v(n)$ divides $v(n+2)/v(n+1)$ is a bit tricker. If you want to know more, you can play around with these terms in the factorised form and try to get an intuition for why this should be true.

@lucid pasture

T0lgi01

Hi and sorry I just saw this ahaha, thank you so much for the thorough and helpful explanation!! that makes a lot more sense 😅 🥰

i dont know how to set up the initial system

is it like kx+y=0 for the first equation?

i dont think thats right bc then the last equation would be 2y-3z=0 but if y and z are 1 then that equation is never true

Can't you just... do the multiplication then get a polynomial in k = 0?

oh like just multiply the matrixs left to right

Yeah

idk what i was thinking

you'll get a 1x1 whose entry is a function of k

i think i was trying to take it as a coefficient matrix or something

so f(k)=0

There might be some neat trick cause ik $x^TAx$ is a common form of things, but I've never learned it

Mosh

thats over my head as of now

im sure theres alot of neat tricks and stuff you can do with matrix and transpose and trace

Yeah, here A is symmetric and diagonalising A makes this much simpler

But that's almost certainly over the top here

Hello - i am trying to utilize the rref command in my MATLAB script but it is not working

Does anyone know why?

It is just printing out the exact same matrix

B = [1 -2 0 0 -9 -8 ; 3 -5 -4 1 -29 -27 ; -1 2 0 1 11 11 ; -4 6 82 -6 32 26];

B([1,4],:) = B([4,1],:);

B(4,:) = B(3,:) + B(4,:);

B(3,:) = -1 * B(4,:) + B(3,:);

B(2,:) = 3 * B(3,:) + B(2,:);

B(1,:) = -6 * B(2,:) + B(1,:);

B(1,:) = 1/2 * B(1,:);

B([3,4],:) = B([4,3],:);

B(1,:) = -2 * B(4,:) + B(1,:);

B([4,1],:) = B([1,4],:);

B([3,4],:) = B([4,3],:);

B([2,3],:) = B([3,2],:);

B(2,:) = 4 * B(3,:) + B(2,:);

B([2,3],:) = B([3,2],:); %REF

B(3,:) = 2 * B(4,:) + B(3,:);

B(2,:) = -1 * B(4,:) + B(2,:);

B(3,:) = 1/37 * B(3,:);

B(2,:) = 4 * B(3,:) + B(2,:);

B(1,:) = -2 * B(2,:) + B(1,:);

B(1,:) = -1 * B(1,:); %RREF

B = [1 -2 0 0 -9 -8 ; 3 -5 -4 1 -29 -27 ; -1 2 0 1 11 11 ; -4 6 82 -6 32 26];

rref(B);

i reset the matrix to the original one stated in the problem to test the command but i have no idea as to why it the rref is not working

what's meant by consistent

check if it has >= 1 solution

any ideas so far

Row reduce until you get something lower triangular, then check for consistency

@nocturne jewel i tried to reduce but all i get is extra baggage whenever i try to do something

im so lost

u know about spans?

but u can write it in matrix form

yes

and I guessing u don't know much about determinants

wdym extra baggage

you should be able to just row reduce it and see if theres more than one solution

which half do you need help with? what have you tried?

I've tried the first half

might be prudent to try a contrapositive argument

but I'm not able to prove the first part

we know that |a+b| ≤ |a| + |b|, so suppose a, b are linearly independent and prove |a+b| < |a| + |b|

actually nah that works but its probably not the easiest approach

how about this

wtf

we want to show $\phi \alpha + \psi \beta = 0$ has nonzero solution scalars $\phi, \psi$; we can divide through to get $\alpha + (\psi/\phi)\beta = 0$ (or if $\phi = 0$ divide by $\psi$ analogously). take the norm of both sides and work from there

???

i just copy-pasted

whatever

Namington

I got norm of alpha + (norm of beta)psi/phi = 0

You can just use the fact that 2 vectors are linearly independent iff one is a scalar multiple of the other. It's the same as what nami said but stated a but more succinctly

I have v1=(a,b,c,d) and v2=(a',b',c',d'), 2 linearly independant vectors from R^4. How do i write Vect{v1,v2}?

what is vect(v1,v2) suppose to denote?

The vector space defined by those 2 vectors

Just span{v1,v2} I suppose

$\text{span}{v_1,v_2}={v\in\mathbb{R}^4| v=xv_1+yv_2; x,y\in\mathbb{R}}$

Mosh

Yes i know that, but it isn't what they're asking actually. Im also kinda confused with their answer, i'll send a pic (its in french tho)

well you asked for the vector space of those vectors so...

{kind=link}

Thats what they're asking as well, but i think we need to be more precise i guess

The value of k for which the linear system 2x+ky+z=4

-kx+2y+2z=2

x+y=0

Does NOT have a single solution.

I found 6. Is this correct?

you can check yourself, you can rref the resulting matrix

what is rref?

reduced row echelon form

RREF the matrix is synonymous w/ using row operations to get it into RREF

Isn't that a long procedure?

"Row operations" oh well I guess my question is answered already

I mean... it scales in complexity as the size gets bigger

but generally a pretty quick algorithm

hey guys, could someone help me prove why non symmetric real matrix can't be diagonalized by any orthogonal or unitary transformation? I just can't get a grip on how to begin at all. (I'm really sorry if this is too trivial and is basically dumb to ask)

prove the contrapositive

so prove that only symmetric matrices can be diagonalised by the aforemrntioned transformations?

Can anyone tell me what "det" means?

'det' means determinant

Ahhh thank you so much.

If I have a symmetric $(k \cross k )$ matrix A, I know it will have a set of orthogonal eigenvector with real eigenvalues. The eigenvectors may be normalized. Now if I construct a matrix $P$ where each colomn contains one of the eigenvectors, how can I prove that it's orthogonal? i.e $P^{T}P = \mathbb{I}$

shadowplayer67

I tried proving $PP^{T}$ by examining what I get from multiplying the i-th row in P by the j-th colomn in $P^T$ but it was nonsensical because I ended up with $\sum_{n= 1}^{k} e_n^{(i)}e_n^{(j)}$ so adding the sum of the products between i-th coordinate and j-th coordinate of the n-th eigenvector. When I instead looked at $P^TP$ ,I got the following sum $\sum_{n= 1}^{k} e_i^{(n)}e_j^{(n)}$ which is just the dot product of the i-th and j-th eigenvector

shadowplayer67

sorry I know it's a lot. I just wanted to show my working/results. I know from $PP^T=(P^TP)^T=I^T=I$ but that feels like cheating because I'm bypassing a proof I can't show. It feels so simple that I don't know what's going wrong

shadowplayer67

If P is an orthogonal matrix then P^t = P^-1 I believe

And P * P^-1 is the identity

sure, but that's the thing.,I KNOW that P^t should P^-1 but I'm wondering why the equality doesn't hold when I decide to expand it in terms of row-coloumn multiplication

The best way to go about this honestly is to work it out with a 2 by 2 example

Think in terms of the inner product, and apply P^TP to the basis vectors

For example, Pe1 is just the first vector in the orthonormal basis

And thus P^TPe1 is just e1, as multiplying any row other than 1 with Pe1 gives you 0 (due to the fact that the columns of P are an orthonormal basis)