#linear-algebra

2 messages · Page 172 of 1

formally speaking, in gaussian elimination, you can only do one step at a time

but for notational reasons we often "combine" steps

when we write them down

since it saves time/space on a page

when in doubt, however, i'd recommend writing them separately.

cool thanks

yeah i was just tryna save time/space but i guess its safer to just do one step at a time

I'm trying to figure out this proof, and where to start really. I'm wondering if I can consider a 1x1 matrix as a scalar as well then just use induction?

Like, by the distributive properties of algebra its pretty easy to prove

But i'm not sure how to relate that to matrices and vectors

the vector has to have n columns

probably write out a general A, u and v, and go through it by hand, cause u+v can be treated as a nx1 matrix

So just do it by case

I wouldnt call it by cases tbh

I mean yeah I could just make a case, but how would I turn that into a proof

You're using a general A u and v

oh i get you

The row number probably

<@&286206848099549185> sorry for the ping but could anyone help me in lin alg, my dms are open too btw cause i will be having to go back n forth with u on the steps

So you should use matrix inversion to solve this

We can write the equation as AB = C

A is the first matrix as asked by question

B is the [0, 5; 1, -2] matrix

C is the [5, 5; -4, 23] matrix

*Since matrix division is not a thing, we need matrix inversion

Because matrices are not commutative, we have to choose left or right inverse

In this case we need B inverse on the right

So A = C*B^(-1)

Calculating that should solve the problem

@fervent gulch Do you still need help with this one

If that is too complex, you can set up an equation with undetermined coefficients

Let A = [a, b; c, d]

And solve with matrix multiplication and algebra

i solved it but i got another question, dm?

Sure

under which circumstances would a $2\times2$ matrix $A$ not be similar to the matrix

$B=\begin{bmatrix}0&1\-\det(A)&\operatorname{tr}(A)\end{bmatrix}$

nix

i can think of the identity and zero matrix but not any others

and in general would those two types of matrices be the only ones not similar to some $n\times n$ matrix of the form

$B=\begin{bmatrix}0&I_{n-1}\**&*\end{bmatrix}$

nix

i think if the characteristic polynomial was $p(t)=t^n+a_1t^{n-1}+\ldots+a_n$ it would be

$B=\begin{bmatrix}

0&1&0&\cdots&0&0\

0&0&1&\cdots&0&0\

\vdots&\vdots&\vdots&\ddots&\vdots&\vdots\

0&0&0&\cdots&0&1\

-a_n&-a_{n-1}&-a_{n-2}&\cdots&-a_2&-a_1

\end{bmatrix}$

nix

Can someone tell me what the replacement theorem actually states

Is it just saying we can take a linearly independent subset of a vector space and add vectors to it to get a subset that generates the whole vector space?

@faint lintel yes

i need advice on how you guys memorize

all these theorems

need some pointers

most of it seems redundant with just extra info

when you walk through them step by step and understand them well, many of them just stick

after seeing them once or twice

yeah theres only two permutations here

yes two

no, it's 2!

your matrix is 2 by 2

yes

anyway

3 * 1 - 2 * 4 is your det

the permutations are (1,2) and (2,1)

as in, well, "first column in first row and second in second raw" and the opposite

hence 3*1 and 2*4. And the latter is taken with a minus sign because that's that permutation's sign.

if we're considering a permutation like 1,2,6,4,3,5

that means we're multiplying $a^1_1 a^2_2 a^3_6 a^4_4 a^5_3 a^6_5$

ConfusedReptile

and for a 6x6 matrix, consider all 6! such permutations, with the right signs.

...and?

why would a 2x2 matrix be, after flattenting, 4x4?

this is 4,, though.

Yes, because you're doing it wrong. You don't permute the elements, you permute the rows, basically.

More precisely, you consider all ways to choose exactly one element from each row (and without choosing the same column twice)

that's N! ways for an NxN matrix, not (N^2)! like it would be for permutations of all elements.

Flattening the matrix is a bad idea, basically. You need that 2d structure.

I don't really get why you'd flatten it at all.

I don't get anything this text is talking about, can somebody help me understand it?

these are the equations for the 3 planes:

this is the graph of 2/3 of the planes (the 3rd plane is not included in the image)

I don't get the (n - 1) dimension (n dimension) stuff

<@&286206848099549185>

pls 😢

a usual plane is a 2D surface in 3D space

you could speak of a 3D hyperplane in 4D space

and so on

think of a point on a line, a line on a plane, a plane in a cube, ??? in ????

you do know, by the way, that real determinant-finding algorihms don't use the N! permutations, right?

fair enough

I'd just make an iterator over the N! permutations, then compute each product and sum them

of course, no idea how much more annoying that'd be in C - I don't think you use iterators much there.

I mentioned it above:

if we're considering a permutation like 1,2,6,4,3,5

that means we're multiplying $a^1_1 a^2_2 a^3_6 a^4_4 a^5_3 a^6_5$

ConfusedReptile

so you just need all the permutations of the numbers 1...N

If you want to make your own algorithm, one way is a recursive one: to get all n-permutations:

- Get all (n-1)-permutations

- For each such permutation, generate

nnew ones, by insertingninto each of thenpossible positions in the permutation.

For example, for 1,2,3. All permutations of 1,2 are [1,2], [2,1]. Insert 3 into 3 possible positions in each:

[1,2] -> [3,1,2], [1,3,2], [1,2,3]

[2,1] -> [3,2,1], [2,3,1], [2,1,3]

So you get 6 permutations of 1,2,3, as you should.

see above. You don't have any "permutations of matrices". You just consider all the ways you can assemble products of elements from the matrix such that you choose exactly one element from each row and each column.

I'd store the matrix as an array of pointers to arrays, yes, but it doesn't really matter. You can do it on a flattened array, too - just transform from the 2d (i,j) coordinates to the positions in the flattened array.

you're still not getting what we are permuting

really, it more like the indexes, pretty much

look at the formula.

We're considering, for an NxN matrix, all possible products of the form

$$

a^{\sigma(1)}_1 a^{\sigma(2)}_2 \dots a^{\sigma(N)}_N

$$

ConfusedReptile

where $\sigma$ is an artibrary permutation of $1, \dots, N$

ConfusedReptile

A sequence of N numbers (1 to N), each of them appearing exactly once, but in arbitrary order.

depends on the specific permutation

you need to consider all the N! of them.

two perms, (1,2) and (2,1)

the first one is when you take the first element of the first row and the second of the second

the second is when you take the second of the first row and the first of the second

well, yeah, it's a 2x2 matrix

no

the i element of the permutation says which element to take from the ith row.

Basically, for a matrix stored as a 2d array, it'd be something like:

fn det(mat: &[&[f64]]) -> f64 {

let mut res = 0.0;

let n = mat.len();

for perm in (0..n).permutations(n) {

res += (0..n)

.zip(perm.iter())

.map(|(i, j)| mat[i][*j])

.fold(1.0, |x, y| x * y);

}

res

}

(in Rust).

untested, mind.

@lavish jewel OHHHH THANK YOU SO MUCH

also how does this plane diagram have too many solutions

ohhh

nvm I got it

this is like a top view

If $V$ and $W$ are vectors spaces, can we talk about a linear transformation $T\colon V\to W$ only if $V$ and $W$ are defined over the same scalar fields?

Ted

no

How would a transformation work if they're defined over different scalar fields?

i'll give you an example

Like, T(cv)=cTv should make sense only if c belongs to the scalar field of both V and W, right?

T is a matrix with complex numbers, but V is defined over the reals

Hmmmmm

Tv is already in the space W, so c belongs to the field over which W is defined

(in this example, anyway)

Suppose V was defined over R, while W was defined over some finite field F. Now, c need not be in F; can we still define a transformation T from V to W?

Mathematics Stack Exchange

Why should linear transformation involve vector spaces over same field?

definition of a linear transformation:

Let $U$ and $V$ be $2$ vector spaces 'over the same field $K$'. So what happens if the

Looks like same fields are required.

it's not required, but the map may be linear over only 1 of the two fields

Although one can use subfields(a subfield of scalar field of W suffices for linear transformation to work).

otherwise, fourier transforms wouldn'T be a thing

anyway. you can specify that T is linear over the field of the input or the output, and that's also fine

T can be linear only in some cases

i have a doubt in linear algebra guys

if subspace is an vector in vector space W which is in V how the axioms identify it?

Huh?

i am confused just learning about subspaces so

oh thanks for that

I'm not sure what you mean by 'identify' it though

like to proove the axioms

You can't prove axioms

You can try to show that axioms hold or don't hold

Although it's little just 'show more clearly' because well....you can't prove axioms

yeah hold or not hold that's the term for it right?

Basically to be a valid subspace

You need the 0 vector

and closure under scalar operations

EDIT under the vector addition too

thanks for the clearance

Essentially you're assuming the vector space is already valid

wym by valid?

And inheriting the vector-operations from there

like if R holds or not ?

valid vector space means

vector addition is associative, commutative, has identity element, has inverse element

those are purely vector-related

And those are, assumed to hold so you shouldn't need to show for them under a subspace of a vectorspace

Alternatively

If you had a subspace of a non-valid vector space

That is a contradiction

And contradictions just mean 'everything goes' (or one result of it is) - like 1=0 kind of stuff

So if that happens you could possibly trace that contradiction to the assumption the original vector space was valid in the first place

wow how long are you praticing linear algebra?

no this is standard stuff >_>

well i am an beginner and i am worst in that

Don't worry about it

If you're a pure math student you need to really get into this stuff

If not you typically 'only' need to master it for R^n

not = applied math, engineering

i am not a pure math student but i might need MATH for my career

Then for you I'd worry more about matrices in general

If you can relate matrices to general axioms of linear algebra great, if not don't worry about it

Guess who passed linear algebra after retaking it the next year ?

you?

Yup and yall wont guess how much I scored😂😂😂

9,5/20

Yeah but 9,5 is considered as a 10

So lmao its fk low

If I had 9,4 I wouldnt pass

well you did had a semester for that course why did you got low?

The problem is my last question was about hermitian matrices,... I had a blackout and completely forgot what that was evn tho I studied it well.

@halcyon pollen as I said, I had a black out

The mast question was on 7 points

blackout damn what happened?

so the subspace axioms are :

- W contains a 0

2.w1+w2 Belongs to W for all w1,w1

3.k.w Belongs to W

those are the axioms?

for subspace vector?

Yes, if W is subset of vector space V then W is a subspace of V if it is closed under addition and multiplication

thanks now i get a context of linear algebra

Can someone show me how to prove that the set of all alternating n linear functions is a subspace?

(cf+g)(a_1,a_2...a_n) is defined as

c(f(a_1,a_2...a_n)+g(a_1,a_2...a_n).

Which is clearly zero if some a_i=a_j

Thanks, I was thinking of showing that all alternating functions are skew symmetric but your solution is much better

how do I know if the rank(2) matrix i computed is a good low rank approximation to use

what are you using it for

Let A be a 5x5 matrix and suppose that det(A)=5. For each row operation (a, b and c), determine the value of det(B), where B is the matrix obtained by applying that row operation to A.

Row operations:

a) multiply row 5 by -3

b) Add -3 times row 2 to row 3

c) Interchange rows 1 and 2

Hey there, I am facing the challange to Prove or disprove the following statement:

dim(V) - dim(ker(f)) = dim(W)

where dim(V) is the dimension of the vectorspace V

what do you think?

As I know that this statement is true I guess it is wrong because it is the wrong sign but i can't find an counter example

Well, your statement would match the theorem if rk(f) = dim(V) right

No because we have a minus and a plus in the other one

Right 😄

That's what is confussing me

Well, it seems in your theorem that f is a function from W to V, but I think in your problem, it might be a function from V to W

but maybe I'm wrong about that

Right, so the statement matches the theorem if rk(f) = dim(V)

so you need to try to find a function f from V to W so that the rank of f isn't equal to the dimension of V

I can't really find any function, because i am not all to familiar with what these actually really mean

Do you understand what the rank is?

Not really sadly

I think that's where you should start

Well it's the dimension of the image of our funtion, but i can't really visualize that and that's where i am struggeling i guess

Like I know all these definitions but that's hard with me

You could look at 3blue1brown's linear algebra videos. Those have good visualizations that might help you

rank is just the dimension of image

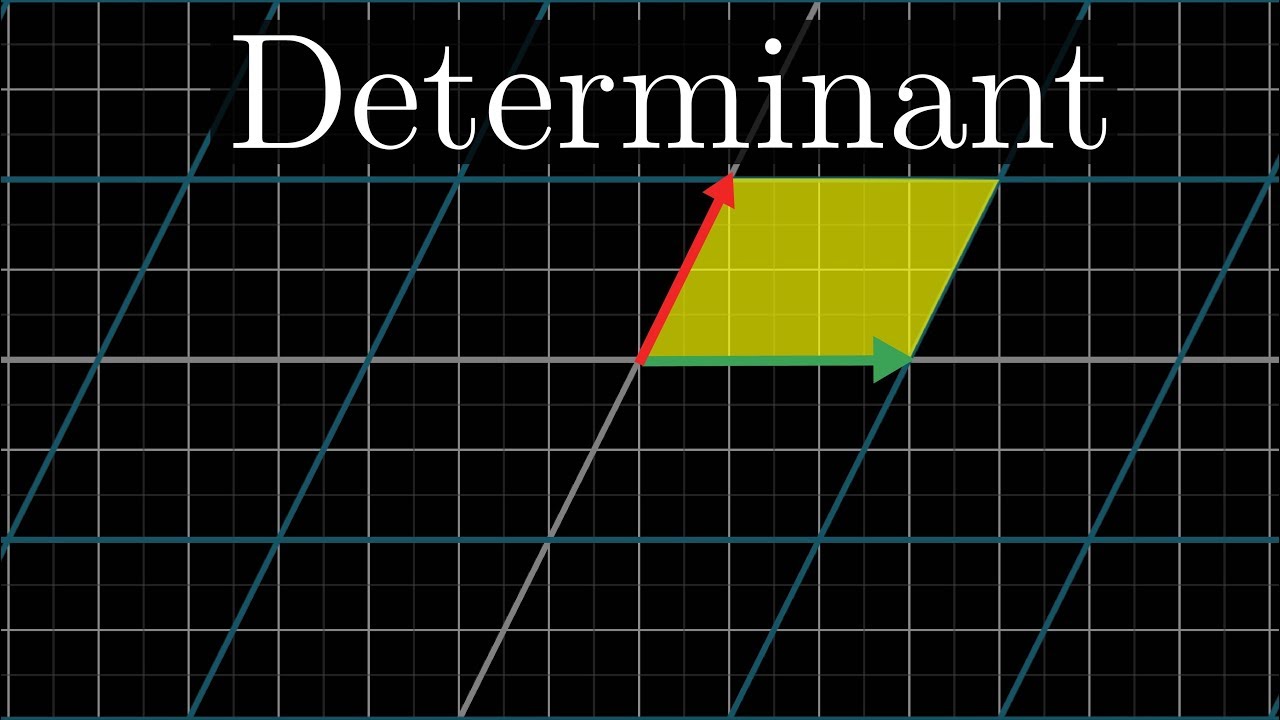

they have many uses

one basic use is to easily calculate the area

Home page: https://www.3blue1brown.com/

The determinant of a linear transformation measures how much areas/volumes change during the transformation.

Full series: http://3b1b.co/eola

Future series like this are funded by the community, through Patreon, where supporters get early access as the series is being produced.

http://3b1b.co/support

--...

How would I reduce this any further?

Would my next step be to just divide r2 by -7 and just have a fraction?

agh

everything that we learned about dealt with the situations where we have a finite set S

idek where to begin with this one

is the goal to show that the basis for V is a subset of S?

the goal is to show that there is a subset of S that is a basis for V

right

should i instead consider the subspace formed by taking the span of S

idk where that would lead me

because then i know i could extend a basis for span(S) to be a basis of V

but

idk

well, since S generates V, you know that the span of S is V

thats what it means for S to generate V

right

Try this idea

so a basis for S would be a basis for V and then i would have to show that this basis is a subset of S

oh

a basis for S doesn't make any sense

er

S is a subset of V, not a subspace

sure thats true

anyways, my idea would be to

take one element from S, if it generates V, then you have a basis (since one (non-zero) element is independent) and you're done

sure

if it doesn't generate V, then add another element from S

i could continue adding vectors from S until i reach n many linearly independent vectors

Depends what you've proven already and have available to use

oh ok

i think i can use this

we did very similar proofs in class so i will check to be sure

my worry is figuring out if this process terminates ? but i have this feeling we already proved that if we have n many linearly independent vectors that are a subset of the vector space, then we have a basis

ty for the help

if you have, then the question is a lot easier

if you haven't, then you might need to do some zorn's stuff

okay we definitely did not mention zorn at all lmfoa

now i am Thoroughly spooked :3

its ok tho

You are so far it makes me feel dumb for my questions lol

I've noticed lol

bro, i get you don't worry lmao

lmao

this is the stuff breaking my brain

I'd say just play around with a calculator

since you need the entries to go away you should start looking at when they go away when you raise them to powers

well for the entries to go away and turn into 0 at ^3 wouldn't it have to be 0

so a would just be a 3x3 of all 0s

not necessarily

do it by hand then

but do what lol

the rare mero sully

express general form for upper triangualr matrix, cube it and set equal to zero all the elements

So for a question like this

I understand that you have to use $\begin{bmatrix} \cos\theta & -\sin\theta \ \sin\theta & \cos\theta \end{bmatrix}$ and then do arcsin(0.6) or arccos(-0.8) to find the angle

chro

the largest vector under the sup norm is x = (1,1,1,...,1,1)

it's just taking the max of all the components

but that also ends up giving the largest coefficients to the matrix multiplication, which is just the sum of elements there

Does something like this count as reduced row echelon form?

no

So then if there is all 0s on the bottom, except for the last column it still wouldn't count as reduced form ?

Or if that 2 was 1 , then would it count?

i don't, understand. STILL

take an upper triangular matrix

write it out

multiply it by itself

what're the diagonal entries?

try to grasp what the product of two upper triangular matrices is gonna look like first

I don't know what that is

(also dont cross post)

do you know what an upper triangular matrix is?

No i don't, i missed one class day emailed my proffesor and he has given me nothing in 5 days.

it's a matrix of the form

hold on let me tex it

$$\begin{pmatrix}a & b & c \ 0 & d & e \ 0 & 0 & f\end{pmatrix}$$

you're gonna tex the general form of an upper triangular matrix?

(T*(Terra), -dτ)

(google is your friend by the way)

oh just the 3x3 case

if i was your professor i'd tell you to check the textbook

anyways

this is a (3x3) upper triangular matrix

can you multiply two of these? what does the product look like?

Ive been trying to understand the textbook and online but i just cant. and all he told me to do is "use letters"

i don't know what you are looking for there, i know you can multiply them but no idea if you mean two of what you put or one of the zero matrix and one of what you put

$$\begin{pmatrix}a & b & c \ 0 & d & e \ 0 & 0 & f\end{pmatrix}\begin{pmatrix}a & b & c \ 0 & d & e \ 0 & 0 & f\end{pmatrix}=?$$

(T*(Terra), -dτ)

this is A^2.

and a 3 is just that times og matrix again

yes.

so i do that then have to row reduce to find a-f?

compare the entries

every entry has to be 0

(as a hint, first look at only the diagonal entries of A^3, your life will be much easier)

i'm assuming it has something to do with the fact the diagonal is gonna be a^3 , d^3 , f^3 by the end?

correct

i really don't wanna do this multiplication for the other spots lol, this is getting gross fast

well now you know that the diagonal entries are gonna be 0 if the third power of A is the zero matrix, yeah?

yes which means a, d and f would all be 0?

yes

now let b, c, e be anything

and just calculate A^3

it's not that hard anymore, most of the matrix is zeros

and you'll easily see the restrictions you need on b, c, e

i really don't, im not smart i'm sorry

thats what i'm working on

yea, this just looks like a lot of letters to me at this point

it should be very few letters

i hadn't done any replacing yet because i didn't think i could yet

the whole point of first finding that a, d, f are 0

is so that your life is easier

once you find that a, d, f are 0

calculating A^3 is extremely easy

why wouldn't you be allowed to?

doesn't it just mean b,c,e are free values. it can be any of them and still work because there is an a,d,f in every single position to cancel them out

yes

yes it does

b, c and e can be anything

there are no restrictions on them

and that's your answer

the 3x3 matrices with anything in those 3 entries and 0 everywhere else are the upper triangular matrices with A^3 = 0

this makes me angry lmao, i already had that answer but thought it was wrong

can someone help me with a true/false

if A is an invertible 2x2 matrix and B is any 2x2 matrix, then the formula rref(AB)=rref(B) must hold

true

elaborate on that

A invertible matrix is a product of elementary matrices

wait it's rref is the identity matrix

So,You can get B from AB via a set of row operations

Now,Just row reduce B to rref(B), Since rref(AB) is unique you get

rref(AB)=rref(B)

i don't feel like that's rigorous enough

have you proved row equivalent matrices have the same rref?

do you know a matrix has a unique rref?

yes

My proof is basically if you can convert a matrix A to some row reduced echleon matrix via row operations,that matrix is rref (A)

because of uniqueness

and you can convert A to AB with row operations

*AB to B

also B is A inverse times AB

yes

anyway,your complete proof can be stated as

"since a matrix is row equivalent to exactly one row reduced echelon matrix and since AB is row equivalent to rref(B),we can say rref(AB)=rref(B)"

i'm still a bit unclear on how AB is row equivalent to rref B

how is AB row equivalent to B? is it just because A is invertible?

now AB is row equivalent to B,because A is a product of elementary matrices and you can cancel each elementary matrix in the product via a row operation

yes it's because A is invertible

How do you calculate the determinant of a matrix nxn when n>3?

there are two main ways: the leibniz formula and the laplace expansion

leibniz; here \sigma and \tau are permutations

laplace; here M_(i' j) denotes the "minor" matrix constructed by taking B and removing the i'th row and j'th column [and i' is simply an arbitrary choice of what row to expand on]

this notation is a bit gnarly and might be hard to wrap your head around

how about elimination and then multiplying the diagonals of the matrix :3

but it gets easier with examples

(which is the same thing, but easier to wrap the head around)

@lavish jewel that works but you need to be diligent in keeping track of what youre doing

since row operations do affect the determinant

what does sgn(t) means?

they just do so in predictable ways

what does sgn(t) means?

sign of the permutation tau

again these formulas are a bit nasty so i wouldnt look too much into the explicit formulae i gave

if youre not already familiar with the concepts

but theres a ton of resources for this on google

which explain it better than can be explained in a discord chat

(trust me, i've tried)

aside from the ones namington has given you, the easier ones to understand are multiplying eigen/singular values, if you are familiar with that

isnt that circular?

maybe i misunderstand what youre getting at

oh wait i was misunderstanding

hmm?

i thought you were computing the eigenvalues directly from the det of the char poly

which obviously wouldnt work

since then... youd still need to know how to take dets lmao

but yeah you can just row reduce instead

as long as you watch what youre doing

yeah, gotta keep track of all the scalings along the way

or go crazy with rotation matrices... oof

im working on markov matrices with this problem and i dont understand how to interpret the eigenvalues lol

my work

its the fourth bullet point... how would i interpret 1 and 1/2 in the context of the problem?

<@&286206848099549185> ?

@heavy coral

You're not told to interpret the eigenvalues

Unless you're asking that question in general, then I must say that's beyond my level (although I can direct you to some readings)

i dont think the eigenvalues have much meaning in general

i mean 1 is an eigenvalue for any markov matrix

and the other is always <1

but i dont think it really tells you anything interesting probabilistically

maybe something about stability conditions or something? dont think it helps you answer bullet point 4 though

oh ok how might i go about the fourth bullet point without referencing eigenvalues

i just assumed because it was the previous bullet point

like is there any other way to conclude some kind of probability?

i'd probably look more to the second bullet point for that; informally speaking, this system seems fairly "chaotic" and the different "paths" the results can go down all produce very different predictions

moreover it doesnt actually give you any information on the final value of the stock, just where it was increasing/decreasing

so its probably not great for predictions

but you'd have to express that more formally, i'd imagine

oo thats so big brain

i was thinking it was the eigenvalues 😔

thank you for the help!!!

They do, the 1st and 2nd in some sense

wdym

I must say I have never used the 2nd eig value

But I always 'knew about it' I guess

yeah i read that an eigenvalue less than 1 is considered unstable, and the second eigenvalue is 1/2

hm

not in your link tho

moreover it doesnt actually give you any information on the final value of the stock, just where it was increasing/decreasing

^This is the definitely the answer to the question, indeed, shows that you shouldn't think too much about eigenvalues all the time

that doesnt seem particularly useful here in any case

Ya

but i'll confess i was unaware of this

I was just referring to the question of 'Stochastic Matrices and Eigenvalues' in general

But yes it's a little more upper level

sure

that was a solid quote @limber sierra

I expect you need more functional analysis to go into it

Which is a bit beyond what I think the question is here referring to, so I didn't mention it until the question itself got solved

ah ok it still makes sense

if theres any value this estimate immediately has to stock prediction

itd probably be some sort of volatility prediction

i think i might leave it out just for safe measure and so i dont potentially confuse my professor

not that he would be confused or anything but--

since we would expect a stock that changes signs more often to be more volatile

but even this isnt really a guarantee

this stock changes sign very often but isnt that volatile

In the end you kinda need the degree

this one doesnt but is volatile

Let me get my sources right actually hmm

turns out predicting the stock market with partial information is hard

predicting the stock market with full information tends to get a lot easier, but it's also kinda illegal

Ok, I was going something more like less math more finance, but couldn't find the essay, so this was what I was referring to

https://people.math.ethz.ch/~embrecht/ftp/VaR_RM_v4.pdf

(or any work by Embrecht on Math. Finance)

My point: essentially the statistic you use changes how your risk is measured - so indeed if you use only sign changes, your risk likely not to be fully captured.

And in a real sense, some risk measures are really 👀 bad

Given that the magnitude of vector a is 10 and the magnitude of vector b is 12 and the magnitude of a+b is 17, find the angle between vectors a and b

how would i do this question?

$||a+b||^2 = (a+b) \cdot (a+b)$

moshill1

or alternatively, cosine rule.

you can draw the triangle, yeah

@torpid portal how would i use cosine law

just

17^2 = 10^2 + 12^2 - 2(12)(10) cos(x)

?

thats the one

oh wait sorry lmao i misread ur numbers

naw you still use cos law just with the numbers corresponding to the angle you want

wait no im stupid it is the angle corresponding to 17

that literally is the angle between a and b

this was correct in the first place

wait how is the angle of 17 the angle between them ?

I mean like I'm sure you can draw a diagram for yourself but

oh

yea youre right

i initally thought it was the angle for 12

so i did sine law after getting the angle for 1

17

why

,ti

The current time for Sneaky is 12:13 AM (AEST) on Wed, 10/02/2021.

u right

sorry in advance if the question is badly formed but I'm starting linear algebra studies and I still don't have some concepts clear ..

I wanted to know, if in my vector I have 1 element equal to 0 then is it considered a subspace? Why? (otherwise why not?)

not exactly one, but the first one is equal to zero

I added the translation to my teacher's notes, did I understand something wrong?

It's a subspace

I expressed myself badly when I first brought you the question?

Set is closed under addition and scalar multiplication

so is it why i can do vector addition and multiplication by a scalar?

Could I still have said it was a subspace if the former had not been zero?

or if in general there was not one equal to zero

I mean that depends on the condition you are imposing

Yes, but it would be subspace with itself it would be R^n

thanks everyone for the answers

You need

(i) addition should be well defined

(ii) multiplication should be well defined

For a subset to be a subspace

Yeah, what moonbears said. There is really nothing more to it. I suggest you do the exercises where you prove certain Vectorspaces to be subspace of a vector space and it will be more clear

we haven't done any exercises yet unfortunately and I'm still looking at the theoretical concepts, but I'll keep this in mind.

Sorry if I continue, but then the example I posted is a subspace also (in addition to the 2 things already said) because 0 is contained in W (the subspace contained in the V space)

right but

technically you dont need to check for 0 specifically

0 is often the most convenient thing to check for

but it suffices to check for any vector v

since if v is in the subspace

v-v must be as well

(because it's closed under + and *)

which means 0 is

I understood what I did wrong with this consideration. I thought that it considered a single vector (therefore a single point with a sequence of n coordinates) but a single vector can be a subspace only if the whole vector is equal to 0. Instead, looking at the recording of the lesson, it specifies that t1 must be = 0 for all vectors that are being compared.

Yup, you can see the subset as the set containing all (0, t1, t2,...t_n) where t are real numbers. From here you can see that you that there are no two vectors in the subset which you can combine with addition to create a vector that is outside the subset.

However if you remove the condition t1=0 then the subset is suddenly the set of all n-tuples(which can be considered points in space R^n) or in other words the set of all (t1,t2,...,t_n) vectors which is just R^n and R^n is a subset to itself and therefore you could say R^n is a subspace to itself but that would be redundant.

quick question. my textbook states that given a square invertible matrix A, Ax=b has at least one solution for each b in Rn, and the linear transformation x |-> Ax is one to one

I'm thrown off by the "at least" phrasing of the first part. How could there ever be more than one solution if it's one to one?

there couldn't

as you say

if A is square and invertible, then Ax = b always has exactly one solution

namely, A^{-1}b

Hi anyone knows a way to do Gaussian elimination easily

I know how it works but is there any way to make it work

Like to easily get my result

Do it right the first time

Wym?

that im aware of there's no easier way w/ gauss jordan

You go through the algorithm of getting to upper triangular, then deal with entries above the diagonal

Aren’t there any strategies

Yes.. the algoritm

Oh ok

Yeah wrote that before I saw the message

Do you know any source that shows how this algorithm is performed

Didn’t know about pivots and swaps should be easier now

UW Seattle's MATH 308, Dr. Ebru Beckyel https://www.youtube.com/watch?v=3XMyUREebN8

{kind=link}

MIT MATH 18.06 Dr. W. Gibert Strang http://www.teachingtree.co/watch/reduced-row-echelon-form-(rref)

TeachingTree is an open platform that lets anybody organize educational content. Our goal is for students to quickly access the exact clips they need in order to learn individual concepts. Everyone is encouraged to help by adding videos or tagging concepts.

hmm http only?

how do I prove that the char polynomial of similar matrices are equal?

from my profs notes

i see this

I don't really see where they got det(C^-1(tI-B)C) though

det(AB)=det(A)det(B)

not that step

we have f_A=det(tI-A)

how do you get det(tI-A)=det(C^-1(tI-B)C)

maybe it's the same property as what you said but idk how

i need that C^-1 tI C = tI

right

And C^-1 I=C^-1

Can someone help me on these 2? This is linear algebra and I do not know how to even start.

How would I figure out the equations for these two questions also what does a horizontal asymptote of -2 mean in terms of the equation

Yeah!

ok

2 questions: do you know the definition of a projection matrix, and do you know what an SVD is

i have a general understanding of svd

(you can use a determinant to figure out the change is "size" when swapping coordinates)

mhm

okay, matrix A isn't given

yup

now, let's call A = ULV^H the SVD of A

U and V are unitary matrices, so that U^H U = U U^H = I, and similarly for V

and L is a diagonal matrix of singular values

we can take A^H (same as transpose for real matrices) and get A^H A x = A^H y

then leave x alone on one side, assuming that Gramian A ^H A is invertible, yeah?

yeah

so we get x = (A^H A)^-1 A^H y

i'll go back and change the name of that

let's call it x_hat

x_hat = (A^H A)^-1 A^H y

and now, A x_hat = y_hat =A (A^H A)^-1 A^H y

and the question is, what does y_hat actually represent

so we SVD the hell hout of that bunch of matrices on the right

A = ULV^H

A^H = VLU^H

okay that make sense

so far so good?

aight

now let's take a look at what is inside the parentheses first

(A^H A)^-1 = (VLU^H ULV^H)^-1

but lo and behold! U^H U = I because U is unitary

oh that's nice

so we get (A^H A)^-1 = (V L^2 V^H)^-1

if we expand the inverse, we get

(A^H A)^-1 = (V^H)^-1 L^-2 V^-1

and then we remember V is also unitary, so its inverse is V^H

so V^H^-1 = V, V^-1 = V^H

meaning: (A^H A)^-1 = (V L^-2 V^H). nice enough

so far so good? we're missing two SVDs to get there

yeah im following

aight

so let's take now A (V L^-2 V^H) A^H = ULV^H (V L^-2 V^H) VLU^H

we get those 2 identity matrices there, since V is unitary

that leaves us with U L L^-2 L U^H

but L L^-2 L is also an identity mat, since L is diagonal

meaning that, finally...

A (A^H A)^-1 A^H = U U^H

where U is a unitary matrix that contains orthogonal vectors that span the column space of A

and now, we bring up the definition of a projection matrix

an orthogonal projection matrix satisfies that P = P^H = P^2, i.e. it has hermitian symmetry and is idempotent

so let's test this out

(U U^H)^H = U U^H, sure enough

and (U U^H)^2 ) = U (U^H U = I) U^H = U U^H

so A (A^H A)^-1 A^H = U U^H is an orthogonal projection matrix onto the column space of A

there must be faster ways of showing it, but using SVDs for this is pretty straightforward due to all the nice properties they have

No this is perfect, i just skimmed over a chapter on SVDs and this seems nice and straightforward

thank's for doing all that haha

i assumed the matrix was full rank here, but you can do the whole procedure with the "economy size SVD" if it's rank deficient. same meaning

just gotta be careful that in the economy case, U^H U = I, but U U^H =/= I

okay

straightforward consequence of no longer spanning the whole space

and yeah it's full col rank

I have another, much more simple question about a problem if you have the time

So I have the Nul and Row span's calculated

and I obviously cant add them because they are different dimensions

Do i just need to use an identity to put it into a form to add the two vectors?

umm, the Nul(A) vectors are in the form 4x1 and the Row(A) are in the form 1x4

ah

so i cant add them

you forgot the first rule of "modern" linear algebra

all vectors are column vectors

ahhhh

or, in other words, the row space is actually the image of A^T

aight

what is the difference between algebraic and geometric vectors and could someone give an example to show the difference

please @ me if you respond

<@&286206848099549185>

Any tip for graphing 3D Sufaces ?

It is getting kinda hard for me

algebraic vectors are the elements of a vectorial space

Do you know what a vectorial space is ?

not really

Well, if you have a set S such that:

Then S is a vectorial space and has some interesting features

Algebraic vectors are just set of numbers in a certain order, considered part of a vectorial space with its operations defined

In R^n they are seen as the same but geometric vectors kinda make no sense in finite polynomial vector spaces nor in the finitely generated vector spaces of continuous functions etc.

the addition operator can be redefined as long as it fullfills the listed axioms afterjack posted

could you give me an example of an algebric vector and an example of a geometric vector i think ill understand the difference there @digital bough

In fact, as ds said that vector can be thought in both ways

I guess that you should take a look at vectorial spaces and linear dependency. I promise you that is it worth

The typical distinction is that geometric vectors are viewed as arrows in space which you can add together (tip to tail), cross and dot products, as scalar multiples.

Algebraic (also called Cartesian) are the purely algebraic representation, which basically takes a point on the plane / in 3D space and associates a vector arrow from the origin to the point in space

so would < 1, 2 > be a algebric vector

Cartesian and Geometric are 2 sides of the same coin, both being vectors in space

Yes

would resultant vectors be geometric vectors?

resultant vectors is the result of adding/subtracting/scaling vectors

so they can be both geometric or cartesian, but you'd typically hear resultant w/ geometric more

and to go back to R^n, R^2 for example is the xy plane, R^3 is 3D space

in this example

vector v is a algebric vector

and vector w is a geometric vector?

The [1,2]^T would be a cartesian, and 30N[E35N] would be geometric

^T just means make it a column not a row tl;dr (This is massive oversimplification of what ^T means, but for this case it's sufficient)

cartesian means algebraic right

yep

so the only difference between geometric and algebraic is that algebric vectors are defined as points on a graph or plane and geometric vectors are defined as quantities with direction

is that right?

Pretty much, yes

could you explain this

Geometric vectors are more associated with the geometric operations (v+w is adding tip to tail)

Cartesian vectors are more associated with points in R^n

$[a,b]^T = \begin{bmatrix} a \ b \end{bmatrix}$

moshill1

Explaining more goes beyond the scope of high school vector stuff, but if you're interested I can explain

that would be geat

so (a,b) are the x and y components right so that [x y] is the matrix thing

^T is called the transpose operator and all it does is it takes a matrix as its input it spits out a matrix with the rows becoming columns and vice versa

a matrix doesnt necessarily represent a bunch of vectors

so how would you read that matrix as

You'd just say it's a matrix

but dosent the matrix represent points?

Conceptually I find the transpose of a vector slightly confusing

they dont represent points; that's vectors

It makes me want to think of everything as a matrix, including the 1x1 matrix

I wonder if that's just a notational convenience

so would that be 6 units right, 5 units up and 0 units diagonally @limber sierra

would what be?

you mean the transformation that vector represents? no

so what is that matrix representing?

"matrices represent linear transformations

[9:52 PM]

or systems of linear equations"

$\begin{pmatrix}6&10\5&3\0&2\end{pmatrix}\begin{pmatrix}x\y\end{pmatrix} = \begin{pmatrix}6x + 10y \ 5x + 3y \ 2y\end{pmatrix}$

Namington

so it'd be the linear transformation that maps an (x, y) vector from the 2d plane to (6x+10y, 5x+3y, 2y) in the 3d plane

they give the coordinates of the 3d vector that you get

when you apply this matrix to (x, y)

for example, if you apply this matrix to (3, -1)

the resulting vector is (18 - 10, 15 - 3, -2)

that is, (8, 12, -2)

so this matrix maps (3, -1) to (8, 12, -2)

the first vector is of course a 2d vector whereas the second is 3d

that's fine

yes.

so lets say we have a matrix of just (1,2) and we wanna map out (3,-1) on it

how would we do that

$\begin{pmatrix}1 \ 2\end{pmatrix}\begin{pmatrix}3\-1\end{pmatrix}$ doesn't make sense, you can't multiply column vectors; however, [\begin{pmatrix}1 &2\end{pmatrix}\begin{pmatrix}3\-1\end{pmatrix} = \begin{pmatrix}1 \cdot 3 + 2 \cdot -1\end{pmatrix} = \begin{pmatrix}1\end{pmatrix}]

Namington

this isnt a particularly interesting linear transformation

yes; since we have a 1x2 matrix times a 2x1 matrix, the product is a 1x1 matrix

which would represent a vector from R

so its a 1d vector

again, the product of two column vectors doesnt make sense

they have the wrong dimensions for you to multiply them

[you can take dot/cross products but those are different]

For multiplying matrices, you need the # of columns in the 1st to equal the # of rows of the 2nd

what if instead of 3,2 we had 3,2 and 10,1 multipled by 3,-1

Namington

Compile Error! Click the  reaction for more information.

reaction for more information.

(You may edit your message to recompile.)

sure

they have the right dimensions

since the first one is 2x__2__ and the second is __2__x1

those match

so we can multiply them

and when we actually multiply these matrix together what are we essentially doing?

like what is that matrix multiplied by 3,-1 represrnting just the transformations?

basically

it's just convenient notation for linear transformations

the original motivation for the definition of matrix multiplication comes from using them to represent systems of linear equations

for example

consider the system[

\begin{cases}

5x + 3y + 4z = 2 \

-2y + z = 1 \

x + z = 0

\end{cases}

]

Namington

it's pretty inconvenient to write out teh full notation every time we want to write out a system

so instead we come up with convenient notation for it:

yea we would just solve it through subsutition and stuff

[

\begin{pmatrix}5&3&4\0&-2&1\1&0&1\end{pmatrix}\begin{pmatrix}x\y\z\end{pmatrix} = \begin{pmatrix}2\1\0\end{pmatrix}

]

Namington

and you can see how our definiiton of matrix multiplication makes this matrix equation correspond to the above system

each "column" of the left hand matrix represents one variable

so the first column is the x's

the second is the y's

the third is the z's

and then taking the matrix product with the (x y z) vector makes us add them all together, i.e. turns them into a linear expression

this works even for "missized" systems

for example

if we added another equation:[

\begin{cases}

5x + 3y + 4z = 2 \

-2y + z = 1 \

x + z = 0 \

2x + 2y - 2z = -15

\end{cases}

]

Namington

we could adapt:[

\begin{pmatrix}5&3&4\0&-2&1\1&0&1\2&2&-2\end{pmatrix}\begin{pmatrix}x\y\z\end{pmatrix} = \begin{pmatrix}2\1\0\-15\end{pmatrix}

]

Namington

note that we have the same amount of variables so we didnt have to resize the (x y z) solution column

we just needed to add another row (another equation)

NOT another column (another variable)

so then how do we solve for the values of x,y,z using matrix

there are various ways; the conventional one is to set up an augmented matrix and row reduce.

could you show me one

(Basically elimination method but quicker)

there are various videos on youtube, its kinda awkward to show off in a discord setting

the key term to google is "gaussian elimination"

sorry if im asking for alot of steps its just that ive learned more in the last 15 minutes then in the 2 weeks of class

Thanks to all of you who support me on Patreon. You da real mvps! $1 per month helps!! :) https://www.patreon.com/patrickjmt !! Thanks to all of you who support me on Patreon. You da real mvps! $1 per month helps!! :) https://www.patreon.com/patrickjmt !!

Gaussian Elimination. Here we solve a system of 3 linear equations with 3 unknowns u...

For small hand-crank problems with 2/3 variables, your eyes are faster

naturally when learning it'll take longer

but you want to get the feeling of what RREF is doing

but when computers solve systems of linear equations

(which is done very often in, say, computer graphic rendering in movies/video games/etc or when setting up statistical models in machine learning or finance)

they do this process

since its faster than substitution and a more "clean" form of elimination

oh i see

also is there a way i can save this convo so i dont forget everything later

right click -> Copy Message Link but

i think it reuires enabling something in discord settings

first

oh okok got it

thank you for all the help @limber sierra @nocturne jewel

im gonna go to bed now but i learned alot more here than in class lol

How would i find the transformation of a reflection across a diagonal line through the first octant in R^3. I have drawn it out and i can visualize it

I want to transform any vector v so that for transformation F, Fv results in a reflection where the head of v is reflected across the diagonal i described

<@&286206848099549185>

A linear operation like that is determined by what it does to the unit vectors

so you can compute the transformation for the unit vectors, and use the result as the columns of your matrix

Okay that makes sense

I'm a little lost on putting the transformations into numbers

mainly because it's in R3

well one issue is that when you say diagonal line, it's not clear if you mean plane

Not a plane

so what would you get if you flipped (1,0,0) across your line?

yeah haha [0, 1 , 0]

then do the same for (0,1,0) and (0,0,1)

ahh

then your transformation is the matrix [T(1,0,0), T(0,1,0), T(0,0,1) ]

where those are the columns

so it sounds like you'd have [ [0,1,0], [1,0,0], T(0,0,1)]

yeah

ya

a bit more abstract of a question, but if I were to draw a line between the initial point P and it's transformation P', that line PP' would be orthogonal to the diagonal line though the octant?

yeah I mean that sounds like the definition of reflection

haha okay fair enough

isn't that transformation more of a 'rotate 180 around this line'

oh okay lol

sorry i should have said that from the beginning

okay so I'm doing this problem

a is very easy to prove and right now I'm working on b

I had the idea to write $m(v) = \langle -i \Gamma v, -i \Gamma v \rangle$ for the standard euclidean inner product

bacono

and from there you can obtain $\langle \Gamma v, \Gamma v \rangle = \langle \Gamma L v, \Gamma L v \rangle$

bacono

I'm trying to prove that L is a lorentz matrix, but I'm not sure if I'm just missing some nice property of orthogonal matrices or something to get the property I need

okay yeah from here if you substitute $v = \Gamma w$, since $\Gamma = \Gamma^{-1}$ we obtain $\langle \Gamma L \Gamma w, \Gamma L \Gamma w \rangle = \langle w, w \rangle$

bacono

$\left[\begin{array}{ccc|c}

-k&1&0&1\

0&-k&1&k\

k^3&-3k^2&2k&k^2

\end{array}\right]$

nix

what would be the most efficient way to solve this system?

a particular solution is really the priority as the null space is already known

looking at the middle row

er wait i thought there was a simplification you can do, never mind

hm

i mean surely if you just want a single solution, fix k = 0

or k = 1 or whatever

k = 0 is probably the fastest since your bottom row immediately zeroes out, and then the above two rows are easy to analyze

k is a known value not a variable, sorry should have mentioned

ah

i mean in that case i cant immediately see any optimizations

besides just plugging in k

unless you mean k is fixed but not known

ah

okay then, dividing through rows by k is probably a good bet

or pwoers of k

like you can immediately get $\left[\begin{array}{ccc|c}

-1&1/k&0&1/k\

0&-1&1/k&1\

1&-3/k&2/k^2&1/k

\end{array}\right]$

wtf did i break

Namington

since we know there is a null space, the first two rows are independent, and a solution does exist, can we disregard the third row entirely?

no?

oh wait i see what youre asking

uh

my matrices-as-systems intuition is pretty weak nowadays

but that makes sense

er actually no

we might not be able to disregard the third row

specifically

even if the first two are linearly independent?

Your system might be inconsistent

that is generally true, but in the situation where this problem originates a solution is guaranteed

i.e. finding a generalized eigenvector

so in general tho row reduction is as good as it gets for something like this?

I'm doing an interesting problem.

Let $X_{1}, \ldots, X_{N}$ be i.i.d withdistribution $\mathcal{N}\left(0, \sigma^{2}\right)$and let $X=\left(X_{1}, \ldots, X_{N}\right)^{T}$. Furthermore define

$$

\tilde{X}{i}=X{i}-\frac{1}{N} \sum_{j=1}^{N} X_{j}

$$

and $\tilde{X}=\left(\tilde{X}{1}, \ldots, \tilde{X}{N}\right)^{T}$such that

$$

\hat{\sigma}^{2}=\frac{1}{N} \sum_{i=1}^{N} \tilde{X}_{i}^{2}

$$

- Show

$$

\tilde{X}=\left(I_{N}-\frac{1}{N} \mathbf{1} \mathbf{1}^{T}\right) X

$$

- Show that the symmetric matrix

$$

B=\left(I_{N}-\frac{1}{N} \mathbf{1 1}^{T}\right)

$$

has the eigenvalues $1$ withmultiplicity $N-1$ and $0$ with multiplicity $1$.

Hint: Thematrix determinant lemmagives

$$

\operatorname{det}\left(c I_{N}+b \mathbf{1 1}^{T}\right)=(1+b N / c) c^{N}

$$

Find the characteristic polynomial for $B$.

- Show by diagonalization that $B=Q Q^{T}$ for an othogonal $N \times(N-1)$ -matrix $Q$. ( $Q$ being orthogonal means $Q^{T} Q=I_{N-1}$.)

¬shm

I'm at the 3rd sub-problem. What to do here?

what does space mean here? (Book:vector calc, Linear Algebra-a unified approach by Hubbard&Hubbard, page 199, topic: interpolation and the dimension formula)

set?

Set which is a vector space

how is a polynomial a vector?

The set of all polynomials of degree<=k is a vector space

And that set is what hubbard means here

Check the vector space axioms

It clearly satisfies the abelian group part

and the 4 scalar multiplication axioms work too

ok here is the definition of a vector subspace

A non empty subset $V \subset \mathbb R^n$ is a vector subspace (or simply subspace) if it is closed under addition and closed under multiplication by scalars.

ElonMoist

it is defined using vectors

That's a subspace

If you ALREADY have a vector space,A subset which satisfies that is a subspace

does that answer this question 🤔

because it says $p \in P_k$ where is $p$ is a polynomial

ElonMoist

A vector space is different

I haven't seen any definition of just "space" in the book 🤔