#linear-algebra

2 messages · Page 98 of 1

iff finite dimensional

yea

Take $(e_1,\hdots, e_n)$ to be a basis of $V$, and define for each $e_i$ a linear functional $\epsilon_i:V\to F$ by $\epsilon_i(e_j)=\delta_{ij}$.

mart:

whats delta

claim: that gives a basis for V^* and consequently dimV=dimV^*

kronecker delta search it up

okay so its like a function that outputs 1 if matrix

sqaure

and 0 if not

square*

?

identity/

the identity of dimension i*j?

yea

i got it

okay

okay i got the proof , for each element in the basis define a linear functional that sends to the corrosponding entry of the identity

thats a basis for the dual

right?

what i read was thtat the delta_(ij) is the ith,jth entry of the identity matrix of dim ij

thats what i meant if i phrased it wrongly

δ_ij is just a shorthand for 1(i=j)

hey,

could someone help me find this permutation`s inverse?

is it just 1, 2, 3, 4, 5, 6

no?

what is it then?

can give $\sigma$

deekaan:

once you have sigma it's pretty easy

just write it backwards

i dont understand.. wym by having sigma

deekaan:

yes

then do like mo2men said and turn that around and you're done

so when i get the inverse does it go like (1), (5,2) and so on?

yes

how would you write in the form i sent here at the beginning

1 leads to 1, 5 leads to 2 and 2 leads to 5

how do you write that?

just flip it bro

up becomes down and down becomes up

no you have to flip it

yea but still

but 5 is mapped to 2 and 2 is mapped to 5 in the inverse.. cant i just write it in ascending order

$\sigma (\sigma^{-1}(5))$

deekaan:

actually it does work

sorry

ya you can just keep it like it is

because 2 and 5 are the only elements that change

and they map to each other

so it equals to its inverse yeah?

yes

@torn silo I had my exam yesterday bro

I got 75%

A Parametric Matrix destroyed me lol

Thanks a lot !

is this a thank you thank you or a fuck you asshole thank you?

I could have gotten a 100% if it wasnt for that parameter

Could have gotten is well written ?

ya it's fine

Oh

and really well done

Maybe if you want I can send you a pic of the parametr I got

I dont know why it was SO hard

I spent 1/2 the test doing it

sure

I do not know how to do Latex matrix lol

$\begin{pmatrix}

1 & 3 & \alpha & -2\

\alpha &11 &8 &-3 \

1 & 18 &14 & 1

\end{pmatrix}$

AfterJack:

Its so simple....

I can not still find the way to solve it

You need to find a value for a that made the system with infinite solutions

Now that I m looking it better I could have switched columns

hmm that isn't so simple

I mean the matrix is pretty tricky

one trick for the future

if you add the third row twice to the first and three times to the second

then you have the first condition for infinite solutions

now all you have to do is find alpha so that the two upper rows become linearly dependent

it's a bit cheesy but using those kinds of tricks you can avoid doing a lot of arithmetic

@gritty frigate

Do I need to understand prealg-alg to understand linear-algebra?

Alright just want to make sure I am doing it right

Yeap, that's fine. Focus on getting comfortable with basic algebra. The elements of linear algebra are easy to understand with a basic understanding of set theory but it's better to have a strong background since linear algebra is pretty abstract.

I agree with  Foundations are important. Make sure you are good with basic arithmetic, linear equations, and functions before you hop in to linear algebra. Having a background in calculus can help, but only in that things like the derivative are secretly linear transformations.

Foundations are important. Make sure you are good with basic arithmetic, linear equations, and functions before you hop in to linear algebra. Having a background in calculus can help, but only in that things like the derivative are secretly linear transformations.

Yeah I am starting off with basic Arithmetic in KhanAcademy although I have learnt it before its just pretty foggy with so much time going by without using advanced math.

Not to worry. The more you do it, the easier it gets.

On the other hand, there are a few books out there that focus on teaching linear algebra in 2 & 3 dimensions alongside geometry. If you really do want to get a taste of linear algebra without the full force of the abstraction, you can certainly use those books.

A line segment has one end point A at (-3, 5) and a slope of -2/3. State Two locations (x, y) of the other endpoint B.

Yeah I got the gist of linear algebra as I study them using vectors and matrices

@slender marsh "Two locations (x,y) of the other endpoint B" ?

I assume that this question is asking you to find two possible points that could be endpoints of the line segment. In that case, what have you tried?

idk what to do

Well, okay, take this to #geometry-and-trigonometry first, it probably belongs to that channel.

given a vector space V with vectors w,v, u; is there a more abstract/general name for vector-addition

f: V \rightarrow V

f(u,w) = v \in V

??

(there are vector-additions that don't look like regular old addition, yeah?)

If you want, you can refer to vector addition in a vector space as $+_V$, where $V$ is the set underlying the vector space.

Abhijeet Vats:

That will probably be helpful in distinguishing between vector addition & the addition on real numbers.

Also, no. The map you wrote above is an incorrect representation of vector addition. It is actually:

$+_V: V \times V \to V$

$(u,w) \to v$

Abhijeet Vats:

they don't care because most vector additions act like regular addition?

or

they dont care because it doesn't matter that much?

(i'm reading a pdf where the vector addition and scalar multiplication are defined using symbols that i rarely encounter)

In many ways, vector addition is very much like regular addition. There are ways in which it is not.

The formalism does matter but it's very rare for it to come up in many problems. Like, when you're doing addition on R, you rarely think of yourself as using a map to associate a real number with a pair of real numbers. You usually just do the addition straight away

So, it's the same story over here

Can you show me the pdf?

Axler doesn't make a big deal about it, and just uses the standard notation that I always encounter.

this author wanted to make a point: http://faculty.etsu.edu/joynerm/documents/VectorSpaces.pdf

He makes a very valid point at that. This isn't just regular addition.

goes through the pain of using abstract symbols, but stays in the real field 😆

linear algebra over the real numbers and complex numbers look pretty different from other fields

Even though these axioms stay the same, some of the theorems can differ

linear algebra over the real numbers and complex numbers look pretty different from other fields

@sonic osprey i'm sure that's true, but axler said dont worry about it.

When you begin learning some abstract algebra, authors tend to use $\circ$ to denote binary operations on sets. Once it's clear that we must disassociate the symbols from their typical meanings, some authors start using + or whatever.

Abhijeet Vats:

I mean, so its still important to look at abstract vector spaces like this, but the trouble of working over general fields is a lot more difficult

I think I need to calculate the vector that spans the null space of a given matrix. How do I do this? This is the line in my notes but I'm very confused, they also seem to have transposed a vector?

aight, thanks for the discourse folks. I don't know how deep to dive into abstraction, so this sanity check has been helpful.

(im a math noob, i'm more used to concrete things like physics 🤪 )

It'll stick to you over time. Just work with it and you'll be okay.

tyty

@autumn basin Can you post the entire question?

(battery's about to run out so i might not be around to help)

You can make very odd vector spaces.

But Axler never will.

well so this is the entire relevant portion of the lecture notes, I'll also post the matrix I need to consider

and my matrix is

8 0 2

0 8 2sqrt15

2 2sqrt15 8

(Not sure how to format that with latex, sorry 😦 )

For context, this is probability but I'm required to use linear algebra concepts here

Let $T_{\Sigma}$ be the associated linear map of the given matrix $\Sigma$. A very quick calculation shows that:

$T(x,y,z) = (x+2z,y+3z,2x+3y+13z)$

If we set the above to 0, then we get $x = - 2z$ and $y = -3z$. So, we are essentially looking at a space of vectors of the form $(-2z,-3z,z) = -z(2,3,-1)$. In other words, the space is made up of scalar multiples of $(2,3,-1)$.

Abhijeet Vats:

@autumn basin

Ah so is your use of T there analogous to the lecturer's use of T that I thought meant transpose?

In that case your explanation makes sense

No. Your professor is using T to denote the transpose of the given vector. I'm using T to denote the linear map associated with your matrix.

yeahh true

In that case, the vector he wrote is a 1 x 3 matrix & he needed a 3 x 1 matrix because that's the only circumstance where the multiplication would make sense

ah right I understand now, the need for the transposition is because of "Theorem 46" which basically just wants you to take that null space vector, and do T* sigma* T transpose

er I used T but I mean (2,3,-1)

Well, technically, it's $\Sigma \cdot (2,3,-1)^T$ but yea

Abhijeet Vats:

$\Sigma$ is the matrix. $T_{\Sigma}$ is the linear map associated with the matrix. They are intimately connected but they're not the same thing.

Abhijeet Vats:

seems like taking a linear algebra module this year would've helped quite a lot with this, huh

thanks for your help mate, think I understand what I need to know 😄

Indeed, a linear algebra class would've been useful for a module which requires linear algebra

who would've thunk

You're welcome.

They're saying the two equations above are both equal to the underlined one, and derive the eigenvector from that assumption. How does one come up with this y = (1-i)x? What is the process to finding this? I'm able to calculate whether they're indeed equal to it, but I want to be able to find it myself

$(1-i)x-y = 0 \implies y = (1-i)x$

Abhijeet Vats:

the first one, just add y to both sides

$2x+(-1-i)y = 0 \implies y = \frac{2}{1+i}x = \frac{2}{1+i} \cdot \frac{1-i}{1-i}x = (1-i)x$

Abhijeet Vats:

@sour jetty

alternatievely, 2x- y - iy = 0 implies 2x - y = iy, so divide by i and simplify

Oh, I see. Thanks a lot!

Does anyone know how to get from second last line to last line?

Specifically how to calculate Re(B-a|r)

it seems like Im(b-a|r) = 0, but I don't know why

Are there any assumptions about alpha and/or beta?

i.e. What's the statement that's being proven?

This is the statement @eager burrow

Oh, I think I might understand

Is your scalar product in such a way that you complex conjugate a factor from the right argument? i.e. (x, a y) = comp.conj(a) (x,y)

yes

because you swap it and then pull the constant out

(conj(ay), conj(x)) then conj(a)(x,y)

Because then, what's happening is

$\text{Re} (\beta - \alpha | (\beta - \alpha |\alpha - \gamma) (\alpha - \gamma))

\text{Re} \overline{(\beta - \alpha | \alpha - \gamma)} (\beta - \alpha | \alpha - \gamma)$

Lartomato:

pray to god this compiles

Okay, neat! And then, inside the real part, you just have the product of a complex number with its complex conjugate

Hence a real numbah

This is a bit messy, but maybe you get what I mean

(i didn't include the 1/|...|^2 factor)

Wait I'll try to derive this but I don't see how the imaginary part is 0?

I'm not sure what you're trying to derive; do you understand what I'm doing in the equation above?

Awright; so, I'm inserting this $\tau$ (which you called r) into the inequality

Lartomato:

I'm focusing on the first summand, so this part

Oh, so does it make sense to you now?

yea

neat

thanks

np

kunze pisses me off

my poor brain cannot understand his "Of course cj = f(aj)" in the last part

and why f(a) =c1x1+...+cnxn

same lmao

<@&286206848099549185>

quickie

is Hom(V,W) the same as L(V,W)

im looking for psets and i keep seeing this Hom

(L(V,W) is the set of all linear transformations between V and W vec spaces)

whats your definition of Hom, all ring homomorphism?

I believe they are the same but I could be wrong

you should ask experts, but a ring homomorphism satisfies

- f(a+b) = f(a)+f(b) 2)f(ab) = f(a)f(b)

so essentially I think L(V,W) is a subset

of Hom(V,W)

linear maps are the homomorphisms of vector spaces

If an mxn homogeneous system has non trivial solutions then m < n. Is this True or False?

I'm thinking that it is True, since rank = min(m, n) = m since m < n. Then m = r < n which means infinitely many solutions which means it has non trivial solutions. I don't see anything wrong with this statement...

wait nvm, its False, there are counter examples

@elfin ingot L(V,W) and Hom(V,W) are two notations for the same set. Both represent the set of linear maps between V & W

can someone explain to me question 5c?

I do not understand why T(b_1) = T(1) = (t+5)(1)

Since if you take T(b_1) = T(1) = 0 (the derivative of it)

How is it still possible that (t+5) is in the answer?

? Why take the derivative of it?

because the example in the book does it

also a person on yt did the same

I just dont know what I have to do ... so I follow the steps from example and a vid I found on yt but the things dont add up

Maybe you should do a bit of reading up from an actual book? It will be easier to approach such problems if you have a good understanding of the theory

the book is good

I just dont get this point

there is not much more to read lmao

do you know what I am doing wrong?

Okay let me try and show you how you might think about this in an easier way.

Let $p(t) = at^2+bt+c$. Then we know that:

$(t+5)p(t) = at^3+(b+5a)t^2 + (c+5b)t+ 5c$

So, a good way of thinking about what $T$ does is to think of it as transforming the coefficients of the polynomial. In other words:

$T(a,b,c) = (a, b+5a,c+5b, 5c)$

Now, finding the matrix relative to the given bases shouldn’t be too difficult

Abhijeet Vats:

now I know how xD

What they’ve done in their working is to consider the image of the polynomial p= 1. That’s the same thing as setting a=0 and b=0 and c =1. In other words, the image is going to be the vector:

(0, 0,1,5) —-> t+5

but what does the image of the polynomial p = 1 mean?

It refers to the polynomial that p =1 is mapped to under the transformation. A linear map is just a function of a particular kind. It’s no different from, say, f(x) = x^3, for example. So when we say that f(1) = 1^3 = 1, then we can say that 1 is the image of 1 under the map f.

(Of course, they are very different in many ways. The basic principle still applies in both cases.)

I understand the gist of what you are telling me

and there are more ways to the same answer

this is what my book does

It’s exactly the same thing. The rule for how T transforms a general 2nd degree polynomial gives you the images of the basis vectors too

In a survey of 200 students of a school, it was found that 120 study Mathematics, 90 study

Physics and 70 study Chemistry, 40 study Mathematics and Physics, 30 study Physics and

Chemistry, 50 study Chemistry and Mathematics and 20 study none of these subjects. Find

the number of students who study all three subjects.

Does this question fall under linear algebra?

Okay thanks

i will try to understand

For the example in the book, think of it as a map:

$T(a_0,a_1,a_2) = (a_1,2a_2,0)$

Abhijeet Vats:

So mapping coefficients of one polynomial to the coefficients of another polynomial

You're welcome.

Shouldn't the determinent of this be 0

E_2 - 4E_3

Then you have the same equation at the top an middle

sorry if this is the wrong channel, but is there a variant of https://en.wikipedia.org/wiki/Bresenham's_line_algorithm, that is specifically for "discrete" grids that only use the 8 basic directions (NESW, NE SE SW NW)?

Basically my goal is to find which grid cells are between two other cells, in a simpler grid cell. Such as

X1 = 5, Y1 = 5

X2 = 10, Y2 = 5

I want to get a result of 6, 5, 7, 5, 8, 5, 9, 5

or is there a simpler way to determine that I am stupidly overlooking?

maybe check out redblob games

Guide to math, algorithms, and code for hexagonal grids in games

that could give you a starting point

ty will give a read

do you want a formal definition or an intuitive one?

an eigenvector is a vector $v$ such that $Av = \lambda v$, where $\lambda$ is an eigenvalue

Namington:

to entangle this more "intuitively"

this means that, when we multiply some vector v by the matrix A

this is the same thing as just scaling the vector

by a scalar factor we call the "eigenvalue"

yes, eigenvalues are defined by the eigenvectors we scale

so if you think of the matrix A as a linear transformation

it's basically saying "there's some vector v for which A is just multiplying v by a constant lambda"

"then, v is an eigenvector and lambda, the constant, is its eigenvalue"

an example of this might be if we have a linear reflection which "reflects" the coordinate plane about the line y = x

in that case, a vector on the line y = x would be untouched

so Av = v

therefore this would be an eigenvector with eigenvalue 1

meanwhile, a vector along the line y = -x would be reflected "strictly"

but the reflection would correspond to multiplication by -1

Those eigenvalues should be obtained by doing det(A - λI) = 0

like if the white line is the line of reflection, the red line is the original vector v, then the reflected vector is the blue line

(if everything is centred at the origin)

then you can see thsi corresponds to just multiplying by -1

so this red vector is also an eigenvector

but it has eigenvalue -1

Ax = -x

the blue vector is the red vector times -1

mhm, I start to see it's purpose

Can I think it as a way to simplify a matrix for determined vectors?

the matrix job*

sure, although it's perhaps better thought of as "special behaviour" at a certain vector

I think of the eigenvectors as being the nicest basis you could wish for

Sorry for the quesiton I will do but

Can I change columns ?

For example x = y

Specially for parametric equations

I am breaking my head over this proof question

Any help would be greatly appreciated

If V⊆W, then dim(V)≤dim(W)

Where: V and W are subspaces of Rn

suppose B is a subset of V that forms a basis of V. clearly, then B is also a subset of W. what must B be in the context of W?

suppose for contradiction that dim(V) > dim(W). what does the above tell you, then?

you should be able to derive a contradiction

@limber sierra Question

I did it this way

I said that if V is a subset of W, this implies that the basis of V is: (v1,...,vn) and the basis of W is: (w1,.....wk) where both sets of vectors are linearly independent. This implies that n ≤ k and so dim(V) ≤ dim(W).

Is this the wrong approach?

Since V is a subset

It has to have at most k vectors

But could have less than that

Right?

why?

Since it's a subset right

you dont sound very confident of this fact you're asserting without justification

sure, it's a subset; what does that mean?

That every element in V is also in W

so...

So at most V would be equal to W

so...

So this means that the basis of V would be at most equal to basis of W

i think i get what you mean

but youre not really explaining the full chain of reasoning

Yeah I'm not sure how else to explain it, trying to think

let $B_V$ be the basis of $V$ and $B_W$ the basis of $W$. Suppose for contradiction that $\abs{B_V} > \abs{B_W}$. But, since $B_V$ is a linearly independent subset of $V$, this means it must also be linearly independent in $W$. So, $B_V$ is a linearly independent subset of $W$; but it is a theorem that a subset of a vector space is a basis iff it is a maximal linearly independent subset, so $B_W$ can't be a basis, since it is smaller than some linearly independent subset (i.e. $B_V$) and thus is not maximal.

Namington:

contradiction, QED

i was really explicit, you dont have to be that wordy

but that's the chain of reasoning

why is this wrong?

So for contradiction, are we saying P->Q is the same as P and not Q?

I am always confused by contradiction

Namington:

if it's not true that (not P)

then P is true

so we're assuming not P

ie we're assuming dim(V) > dim(W)

Got it

p(t) = -4 - 2t

what is p(-2)? what is p(0)? what is p(1)?

here p is a function

you're not multiplying it by anything, you're evaluating a function at certain values.

oh

i see

wow

So I wanted to clarify what I said earlier - since V is a subset of you don't we know the entire basis of V is in W?

right

So then the basis of W should have at least the number of vectors in V

since V subset W we know B_V is a subset of W

Yes so that's why I was saying n<=k

you skipped all the intermediate reasoning, though

the logic is "B_V must be linearly independent, but then W would have a linearly independent subset bigger than its basis, contradiction"

this proof doesnt have to be phrased by contradiction, fwiw

it could be rephrased another way:

"B_V is linearly independent since it is a basis, and is contained in W since V is a subset of W. the dimension of W is the size of a maximal linearly independent subset of W. so, |B_W| is an upper bound on the size of a linearly independent subset of W. Since B_V is a linearly independent subset of W, this means that |B_V| <= |B_W|"

So you are saying I should explain all of that instead of just stating n<=k?

Just want to make sure

you probably don't need to be quite as explicit as I was.

the point is just that you can't randomly say "therefore n <= k", you have to give some sort of justification

of why these two facts connect

Got it

Much appreciated

What do you mean by maximal linearly independent?

I know what linearly independent is

Not maximal

Okay I just found the definition online

sorry, i just mean "the largest possible linearly independent subset"

maximal means "largest"

No problem, thank you!

you might not have proved that "the dimension of W is the size of a maximal linearly independent subset of W"

but the proof isnt too hard

at least in the finite dimensional case

I have another question I'm working on so if I'm facing an issue I'll post it here

I don't think we have

well here's a quick proof for you:

let B = {b_1, ... b_k} be a basis for W

so dim(W) = k

B must be linearly independent, since it's a basis

Yes

Yeah

since B was a basis, we can write any element of W as a lin. comb. of b_1, b_2, ... b_k

including b_k+1

but this means B' is not linearly independent

since b_{k+1} can be written as a linear combination of the rest of B'

hence B' is not a basis

so, any subset larger than B can't be a basis

therefore, if B is a basis, then it is a maximal linearly independent set

hence dim(W) = |B| = size of a maximal linearly independent subset of W

QED

one notes that this only works "nicely" in the finite dimensional case

but fortunately, subspaces of R^n are necessarily finite dimensional

so you dont have to worry about that

So you are saying because b_k+1 is in span of B that B' is linearly dependent?

Got it, makes sense!

If you don't mind - could I post one more question and have you check my solution?

If V⊆W and dim(V) = dim(W), thenV=W. Suppose that dim(V) = dim(W) and V ⊆ W means that the basis of V: (v1,....,vn) of linearly independent vectors spans V, and also, because V is a subset of W, this means that basis of V lives within W and spans W

So span(V) = span(W)

V = W

"that basis of V lives within W and spans W"

you should probably say "and spans W because it is a linearly independent set of the same size as a basis of W" or something similar

also uh, dont say span(V) or span(W), say

span(basis of V)

but yeah since

V = span(basis of V) = W

V = W

"and spans W because it is a linearly independent set" so what exactly does it being a linearly independent have an affect on this?

I get the same size part of your explanation

well, something like $\left{\begin{pmatrix}1\1\end{pmatrix}, \begin{pmatrix}2\2\end{pmatrix}\right}$ does not span $\bR^2$

Namington:

despite the fact that $\dim(\bR^2) = 2$ and this set has two vectors

Namington:

because it's not linearly independent

for example, you cant write $\begin{pmatrix}1\0\end{pmatrix}$ using these vectors

Namington:

But since it was a basis in V it was linearly independent right

right, in the case of your problem

we know its lin. ind. because it was a basis of V

Should I still restate it?

so this issue doesnt arise

i mean, I would

personally

just to make it clear that that's the reasoning

Got it

Also, could $\begin{pmatrix}1\0\end{pmatrix}$ and $\begin{pmatrix}0\1\end{pmatrix}$

Supreme:

Compile Error! Click the  reaction for details. (You may edit your message)

reaction for details. (You may edit your message)

Idk Latex - um could the vectors (1,0) and (0,1) be a basis of R2?

I don't think it spans right?

Google says: "In fact, any collection containing exactly two linearly independent vectors from R 2 is a basis for R 2"

I'm an idiot - it spans

My bad

those span yeah

ninnymonger:

Or maybe constant functions is a better word here?

yep

Quick, indeed. TYVM

you're welcome

so $\mathcal{P}_0 (\mathbb{F}) = \mathbb{F}$ ?

soαρ:

ignoring some set theoretic stuff, yes

Does anyone know why Pa is that given value?

nvm thats just the definition of orthogonal projection onto compl(W) since compl(W) has degree 1 right

From the equation $f(\alpha) = (\alpha|\gamma) \cdot \frac{f(\gamma)}{|\gamma|^2}$, you can see that you can express $f(\alpha)$ as a scalar product $(\alpha | \beta)$ if you define $\beta$ the way that they do

Lartomato:

You're just pulling the factor $\frac{f(\gamma)}{|\gamma|^2}$ into the right side of the scalar product, which means that have you have to complex-conjugate it on the way

Lartomato:

@wintry steppe does that make sense

What about what he said is confusing to you?

You can express f(a) as a scalar product (a|B) if you define B the way they do

yeah

Go look at the properties of the dot product

especially the one about scalars

f(y)/||y||^2 is just a scalar

Yea I know all the properties its just that I don't know where everything comes together

Okay, well use the property

what do you get when you use that property on the scalar

f(y)/||y||^2 like I just said

You have $ (\alpha|\gamma) \cdot \frac{f(\gamma)}{|\gamma|^2}$

Zopherus:

use the property of the dot product

isn't • just the ordinary multiplication

ordinary multiplication of scalars yes

You said you knew your properties of dot product? There's a property that looks a lot like this

(a, y compl(f(y)/|y|^2))

B is equal to that value right?

And you should think about what B even represents in the theorem

How is B equal to the RHS value?

Look back at your theorem, what property do you want B to satisfy?

Actually I'm not even sure of the meaning of a linear functional

A linear functional is a mapping from a vector space to its underlying field

Beta is being defined as that thing

Typically its a map from a vector back to R or C

a linear functional is a linear function from V to the field that V is defined voer

Linear functional != linear function

I.e., R^n to R

ok, I see, so its saying for every linear functional there is a b such that the linear functional is represented by f(a) = (a|b)?

For a linear function you are correct

Yes, exactly

(its important that V is finite dimensional here too)

And if they define beta the way that they do, then it fulfils that property

so here B is defined as the vector such that <a,b> = f(a), and if b = y*compl(f(y))/|f(y)|^2 this holds?

kind of

The whole point of the proof it to show such a vector b exists with that property

We don't know if it exists, we're trying to prove that it does

And taking the value of b = that makes b have that property, so we know such a value of b exists

oh god

im so stupid

I realized

thanks

do you plug B into the RHS in y to show this?

Ah, they actually do show that b is unique, but not really clearly

I'm not sure what you mean by that

like f(a) = (a|y)f(y)/|y|^2

and do they just let B = y

since they defined f(a) already

Sorry this wasn't clear, I think what I'm trying to say that they are trying to show that f(a) = (a|b) by defining b to be compl(f(y))y/|y|^2 and then replacing y with b

I don't know if this is wrong

Oh right

yea

makes sense

thanks, and they did prove uniqueness using first proof it seems

This is confusing me. Why do they define f to be both the thing that is integrated as defined by the inner product <f,g> AND also the linear functional?

L(f) = f(z) is a notation I don't understand also

and finally I am clueless to why (hf)(z) = 0

if h = x-z

the other parts are ok

L is a function from V to C, where V is the vector space of polynomials with complex coefficients, and C is the complex numbers

so L takes in polynomials, and outputs complex numbers

so if f is a polynomial, then L is defined to be the function such that L(f) = f(z)

Ok, I understand that, now I don't know why (hf)(z) = 0?

do you understand what hf means

not quite, is h h(x) = x-z or h(z) = x-z

Ok, so L(f) = f(z) because a linear operator on a polynomial is still a polynomial?

then why?

So they defined L(f) as f(z)? its not something required?

That is how they defined L yes

I see, and this definition makes L linear

Still I don't know why h(f(z)) = that integral - z = 0?

ok, but it becomes x•(integral)-z•(integral), which I don't see is 0

or I don't know how to multiply them together

it says for suppose we have f(z) = from 0 to 1 of f(t)compl(g(t))

Okay sure

even if it is polynomial, I cannot see why its 0..

No like, I mean

I was confused why z was not a variable

but then realized its fixed

So I was misinterpreting the proof by thinking that L is all linear functionals, instead they just chose 1 of them and showed with that particular L they can reach a contradiction

L is not an arbitrary linear functional correct

thanks again

How do you show the basis used here is orthonormal? and what is the special case of the corollary?

the standard basis for C^{nx1} is orthonormal. The special case of the corollary is the line where they show that the conjugate transpose of A is the adjoint operator. @wintry steppe

oh ok, just a further question to clarify: given any ordered orthonormal basis, and some matrix A corresponding to transformation T, is conjugate transpose of A always the adjoint?

I think thats true right? directly follows from the corollary

isn't that exactly what it says?

npnp

the words here confused me a bit because it says its a special case of the corollary

so I thought maybe there was cases within the corollary to explore

ah yea, ig by special case, they just meant the case when V = C^nx1

Also do you know how they can rearrange like this?

like from 1st line to second line, and subsequently to 3rd line.

is trace of product commutative or what?

yep it is, as long as the multiplication is defined ofc.

so trace of standard matrix multiplication?

is commutative?, but not necessarily self-defined matrix multiplication?

nvm i got it I think, I think I skipped over early sections of the book

idk what u mean by "self-defined" but basically y'know if u have two non-square matrices where the multiplication works one way, it doesn't necessarily make sense the other way.

yea, my question was not well thought

Does anyone know why U1 = (U1)* and U2= (U2)*. Is it because of the property T** = T?

Not really

then why

You should note that this isn't true for all U1 and U2

such that T = U1 + iU2

It's saying that there exists U1 and U2 such that T = U1 + iU2 and U1 = (U1)* and U2 = (U2)*

One thing I'm confused is it talks about self-adjoint T=T*, then suddenly it talks about representing any T linear on complex inner product space as T = U1+iU2

like I cannot see the connection of that to self-adjoint

Given any complex number z, you can represent it as a + bi right

Yea, though a,b real is the whole purpose of doing that

And that's basically what they're saying

self adjoint operators are like the real numbers

T here is a complex operator, its an operator on a complex vector space

So you can write it like T = U1 + iU2

just like you can write z = a + bi

and the property of real numbers is that conjugate of a real number is itself

just like for operators

yea, thanks

Im lost on how this shows B is in W

oh nevermind I get it

its proving that B is also an eigenvector

What are quantifiers in the context of systems of equations?

How does this relate to the concept of free and bound variables

What is the difference between a quantified variable and a bound variable

Hey all

Just checking that x^2+y^2+z^2<=3 describes all points contained in a sphere ?

yes

Seconded

Let's say I have 3 independent linear equations with 8 variables in total. Not 8 variables in each mind you, but 8 unique variables total.

What can be expressed in terms of what else? There are rules clearly. For example, if each variable only appears in one equation, the variables in each equation cannot be related to those in the others at all.

Anyone interested in working through a linear algebra course as a group?

Or know where I can find a group if not

Hi

Prove that dim(U+V) = dim(U) + dim(V) if and only if U∩V={0}

I am trying to prove: if U∩V={0} then dim(U+V) = dim(U) + dim(V)

I am sort of just not sure where to even start

U+V = { u + v | u in u v in V }

find the general case first

let b be a basis of u and b' be a basis of v

how can u write any element in U+V

dimension wise

@wintry steppe

Okay, so just a rough outline of what I am thinking - if we let b be a basis of U and b' be a basis of V, then b + b' - (b∩b') = U + V

Right?

And since (b∩b') = 0

Something like that? @elfin ingot

an element in u would have to be written as n linear combinations and in v as n' linear combinations

n and n' dimension of U and V

and the chance of an element beingf in both

but yea ig ur right

One second, let me think about this

Okay I'll write it out and let you know if I have any questions

sure

@elfin ingot I started off by saying: let (u1,....un) be a basis for U and (v1,....vn) be a basis for V

Not sure what to do next - would I then pick an element u in U and v in V and write them as a linear combination of (u1,....un) and (v1,.....vn)?

this assumes both spaces have the same dimension

yea

Sorry, I mean v1.....vk

do you see why the dimension of U+V can be at most the sum of the dimensions?

Yes, I do

then it suffices to find a set of n+k linearily independent elements in U+V

(this will then be a basis)

Okay, one sec... So now I did u+v = m1u1+...mnun+n1v1+...nkvk -- so this should be linearly independent in U+V?

what is u and v?

I let u be an element of U and v be an element of V -- u1...un is a basis for U and v1...vk is a basis for V

ok, what do you mean by "this" when talk about linear independence?

u+v should be linearly independent?

that statement makes no sense

linear independence is defined for sets of vectors

and a singleton is always linearily independent in that sense

like ${u_1, u_2, \dots, u_n}$ is a linearily independent set for example

Lochverstärker:

(because it is a basis)

you now need to find such a set of size n+k in U+V

||there is an obvious choice||

I see

Okay one sec, I'm kind of losing sight of this problem - so we are given U intersect V is 0 and we want to show that equality

So what exactly am I supposed to do to show this again?

the dimension of a vector space is defined as the size of a basis

Yes

so ultimately you need to find a basis of U+V

That has the same size as U + size of V

a basis is a set of vectors that is both linearily independent and spans the space

yeah

Yes

you are given a basis of U and a basis of V

so it is natural to construct a basis of U+V from that

So just basis of u + basis of v

if + is set union, then yes

well, you still have to prove that this actually is a basis

so that it a) spans the space and b) that it is linearily independent in U+V

huh?

I meant, after I prove the fact that it is a basis

How would I use the fact that U intersect V = {0} satisfies the equation

dim(U+V) = dim(U) + dim(V)

oh, so the other direction?

Wait, I'm proving right now: if U intersect V = {0} then dim(U+V) = dim(U) + dim(V)

yes

Yes

if you find a basis of U+V of size dim(U) + dim(V), you are done

Okay got it, I'll do that

And I need to prove that basis spans and is linearly independent

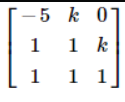

otherwise it wouldnt be a basis

how do i do this?

the determinant is 0 whenever you have linearly dependent rows/columns

Calculate the determinant of M in terms of k, then set that expression to 0, then solve for k

by imagining expanding along the first row or last column (cause there's a 0 there it's convenient) you can tell it's a quadratic. That means it has at most 2 distinct roots for k. Doing what kxrider says by looking at the first two columns and last two rows makes it obvious what they are.

Yes.

does sum mean add?

yes

ok so i add them, then put them back into the original, which SHOULD equal 0?

no way

they just want you to add them, has nothing to do with plugging them back in

it's only 0 when you plug in 1 or -5

no if it's 0 it's linearly dependent

k

plug in k and tell me what the linearly dependent vectors are

x1=-x2

x2=x2

x3=0

no no

if you plug in k=-5 then the first two columns are the same vector

if you plug in k=1 the last two rows are the same vector

that's what's making the determinant spit out 0 by being linearly dependent

ahhh

How about htis one?

Think about how each type of row reduction will effect the determinant of a matrix

And think about how you can row reduce M into A, since the determinant of A is given

Hey everyone

What's this called in english

In french it's Composante

the formula is

(dotP(a, b))/norm(a)

@wintry steppe A scalar projection of b onto a, I think.

thanks

any help for mine? @eternal finch

I've done this before but it's been a while

so all I need is something to jot my memory

oh sorry

Most people here are in uni classes I'd imagine right

on the left you can see this channel is in the "early uni" category

That's the level of math I thought, not necessarily related to the people here

Could someone explain back substitution to me over voice? Specifically this problem

its where you put the system in row echelon form, and then you start from the bottom, z = [something] and plug it into the equation above, solve for y, and then plug in y and z into the top equation and solve for x

@wintry steppe When you have a matrix in row echolon form/reduced row echolon form, you will know which variable's value you can find first.

Then others will follow.

so the spectral theorem says that in the complex case, all normal matrices can be unitarily diagonalized, but are there any matrices that can be diagonalized, just not unitarily so?

because complex numbers are algebraically closed there'll definitely be "enough" eigenvalues

but is it possible that the eigenspaces will have high enough dimension, but there is no orthogonal set of eigen vectors that span the whole space?

Consider an operator defined by the rule

L1(P(t)) = P(t).

How can I find its eigenvectors and eigenvalues and prove that it is not diagonalizable?

umm is it just me or does that look like the identity @placid oracle

Hmm which one

L(p) = p

Prove that dim(U+V) = dim(U) + dim(V) if and only if U∩V={0} - I have hit yet another snag with this question

After picking a basis for U and V and adding them together

I am not sure how to show that it is linearly independent

Well, you still haven't used the fact that U intersect V is {0} yet, so try to use that

How would I use it? if U intersect V is 0 then I know the basis of U and basis of V - their linear combinations - none would be the same

Right?

So let's say basis U is u1.....un and basis V is v1....vn. Then, c1u1+....+cnun+a1v1+...akvk = 0...

I know c1u1 != c2u2 != .... akvk, right?

You can't assume c1u1 != c2u2 here. A counter example would be when c1 = c2 = 0.

I think you are on the right track with the bases

I am just slightly confused how to show c1......ak = 0

To show linearly independent

I've been stuck on this for a while, it's frustrating me :/

but you do know how to show linear independency of vectors, right?

Yes

what's the solution to this?

Show that the relation c1v1+...+ckvk = 0 can only be done when c1...ck = 0

@radiant jasper I am pretty sure that's how to show linear independence

So the issue is I don't know how to show those constants are 0 lol

I don't understand how if U intersect V = {0} should help with this

Since I am proving if U intersect V = {0} then.....

If you don't have that condition then how could you assume u1..un and v1..vl are linear independent

@foggy lodge This is the definition

Oh yes, you're right

Well then if they are linearly independent then we know using that fact the constants are 0

So that's it?

Given that we know U intersect V is {0} we know that basis of U and basis of V are linearly independent

But you have to prove it first right?

||yeah, the basis of the sum will become the basis elements of U and V, because then any element of a basis will not be expressable as a linear combination of the other terms.||

Hmm, yeah but I still don't get how I show the constants are 0

I don't see what information they provided can help me arrive at that conclusion

By they I mean the question

U and V are subspaces of some vector space W, right?

Then that means that U + V is all possible linear combination of all the vectors in U and V. However, we can use a basis of U and a basis of V to find all possible sums, which creates a new subspace

You create a new basis, and at most it can have all the elements in both of the original bases, however, if we can express one or more of the vectors in the bases as a linear combination of the other, i.e. U intersect V being nonempty, then the dimension will be smaller

This is my understanding so far

https://cdn.discordapp.com/attachments/540211747613704221/715423432711471104/unknown.png anyone know how to solve this?

{kind=link}

ill give it a look @sick dragon

U intersect V is empty though so this means that dimension will be the exact same

not quite, this just means that there isnt an element in both of those subspaces

so the basis elements are unique across both of the bases

I see

so if they are unique, all of the elements in both of those bases form a new basis for this new subspace

which means that dim(U+V) = dim(U)+dim(V)

where dim(U) = |some Basis of U|

Ok @sick dragon, what have you tried so far

yeah this isnt in my class slides

I see

so im just trying to remember stuff from calc

Are you familiar with applying matrices to other matrices? I can give a quick rundown

sure

When we have Ax, that represents a linear transformation A being applied on a vector x.

Yeah

Now, if we have BAx, we first apply A to x, giving us x', then we apply B to x'

However, we can represent BA as one composite transformation

When we multiply the matrix B with A, B acts on the ROWS of A. Similarly, A acts on the COLUMNS of B

Therefore, in your problem, we can introduce a new matrix B that does row operations in order to get the modified matrix

The first two rows are the same, so in this newly introduced matrix, we will take 1 of row 1, 0 of row 2, and 0 of row 3

So our first row is 1 0 0

Our second row is unchanged, so we want 0 of row 1, 1 of row 2, and 0 of row 3, so the second row is 0 1 0

Try the third row yourself

0 of row1, 0 of row 2, 1 of row 3. 0 0 1

Not quite

That would just give us the original row

We want 3g+a, 3h+b, 3i+c

How would we get that

Try again

We want x quantity of row 1, y quantity of y, and z quantity of row 3

When we do that, we get x y z

We would scale row 1 by x, row 2 by y, and row 3 by z

Then add them all up

Ok great

So you see, 3g+a, 3h+b, 3i+c is a sum of 3 times row 3 + 1 times row 1

So our bottom row is going to be 1 0 3

We then have

1 0 0

0 1 0

1 0 3

We apply this matrix to matrix A

Since det(AB) = det(A)det(B), we get det(this new matrix)*10

The determinant of this new matrix is 3, so the answer is 30

@sick dragon

Lmfao

This is wrong

Somehow it gives the right answer though lol

My method is the intended one

😄

Honestly if I was the professor I wouldn't even be mad

But just to clarify, you can only pull out scalars from a matrix if you divide ALL of the elements by that scalar

i see

Also that middle step is illegal lol

can i just plot these and take the area

It's a good idea to plot it yeah

since this is linear algebra and you know it's a parallelogram

you should probably use a determinant to compute it

well, triple product gets you volume

Yeah

you want cross product effectively

knowing it's a parallelogram, just subtract one vector from the other three to put it at the origin

one vector should be obviously the sum of the other two

i think im supposed to move it to the origin (dunno why)

so you just take the cross product of those two to get the area

then use determinant 🤷

yep that's what I just said

cool

subtracting one vector from the other 3 is translating it

I think of it as finding the side vectors of a parallelogram because visually that's what subtraction gives you

Though, what's the intuition for taking the cross product

Huh ok

I think it's certainly an interesting thought you have

Because the determinant is a measure of how much you're scaling the volume/area

I never thought about that

However, I think it's incredibly difficult to do that problem that way, and I think the point is to use the multiplicative nature of the determinant function to find the answer

dimension of a matrix M_mn, is the result of m times n. right?